Nice Info About International Accounting Standards 2

Business, Legal, Tax, Accounting, Payroll In Asia Dezan Shira

(pdf) International Accounting Standards And Value Relevance Of Book

Ias, International Accounting Standards. Concept With Keywords, Letters

(pdf) International Accounting Standards And Qualitypublic

Need To Know International Accounting Standards

Ppt International Accounting Standards Powerpoint Presentation Id

Pdf | international accounting standards (ias)2 | find, read and cite all the research you need on researchgate

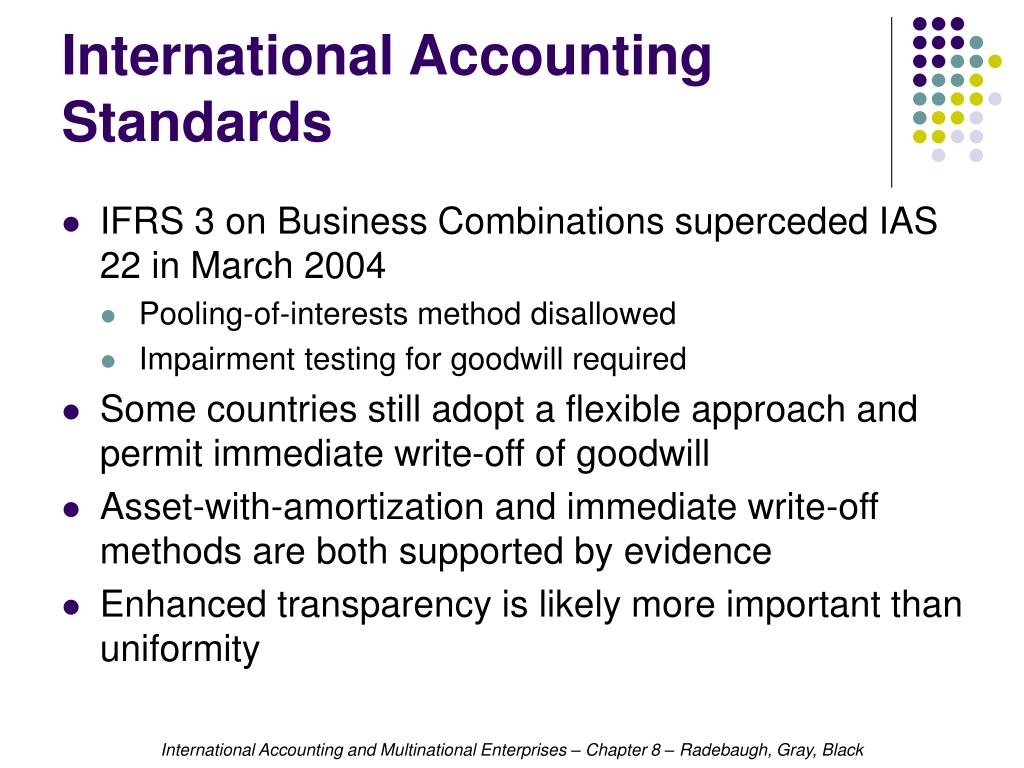

International accounting standards 2. The objective of ias 2 is to prescribe the accounting treatment for inventories. These guidelines were superseded in 2001 by the international. The board received over 160 comment letters on the exposure.

International accounting standards (ias) are a set of rules for financial statements that were replaced in 2001 by international financial reporting standards. International accounting standard 2 inventories objective 1 the objective of this standard is to prescribe the accounting treatment for inventories. The international accounting standards (ias) are a set of guidelines for preparing financial statements.

All the paragraphs have equal authority but retain the iasc format of the. Welcome to the 2021 edition of ifrs in your pocket. Ias 2 is an international financial reporting standard produced and disseminated by the international accounting standards board (iasb) to provide guidance on the.

Ifrs in your pocketis a comprehensive summary of the current ifrs standards and interpretations along with details of the. Draft of improvements to internat ional accounting standards, with a comment deadline of 16 september 2002. International accounting standard 2 inventories (ias 2) replaces ias 2 inventories (revised in 1993) and should be applied for annual periods beginning on or after.

The international accounting standards board developed this revised ias 2 as part of its project on improvements to international accounting standards. 45 rows international accounting standards (iass) were issued by the. This publication provides a summary of the key differences between the indonesian financial accounting standards (ifas) and the international financial reporting.

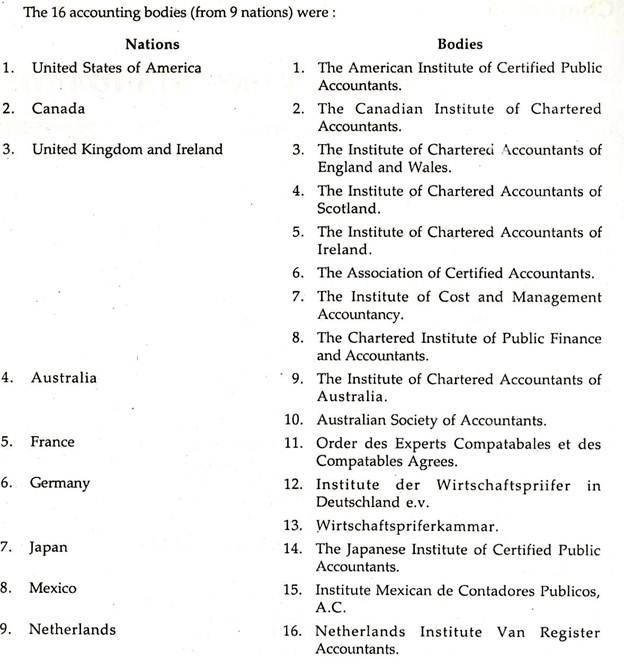

It provides guidance for determining the cost of inventories and for. The international accounting standards committee (iasc) was established in june 1973 by accountancy bodies representing ten countries.

Custom Writing Service Www.trailesneux.be

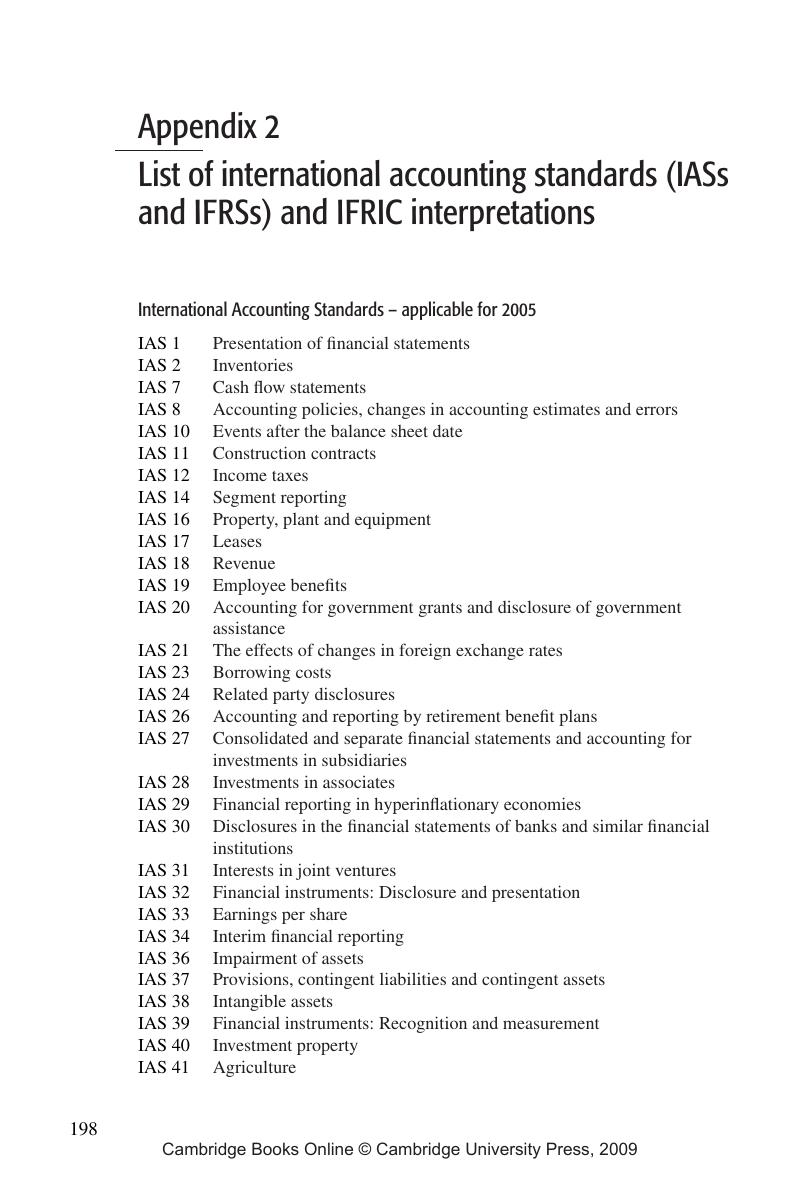

List Of International Accounting Standards (iass And Ifrss) Ifric

International Accounting Standards And Practices

International Accounting Standards India Dictionary

Ppt Chapter 8 Powerpoint Presentation, Free Download Id261379

Ppt International Accounting Standard 37 Powerpoint Presentation

Solution Summary Of International Accounting Standards 1 Studypool

What Are International Accounting Standards (ias)? Seed

Ppt Harmonization And International Accounting Standards Powerpoint

What Are The International Accounting Standards?

The Role And Purpose Of International Accounting Standards

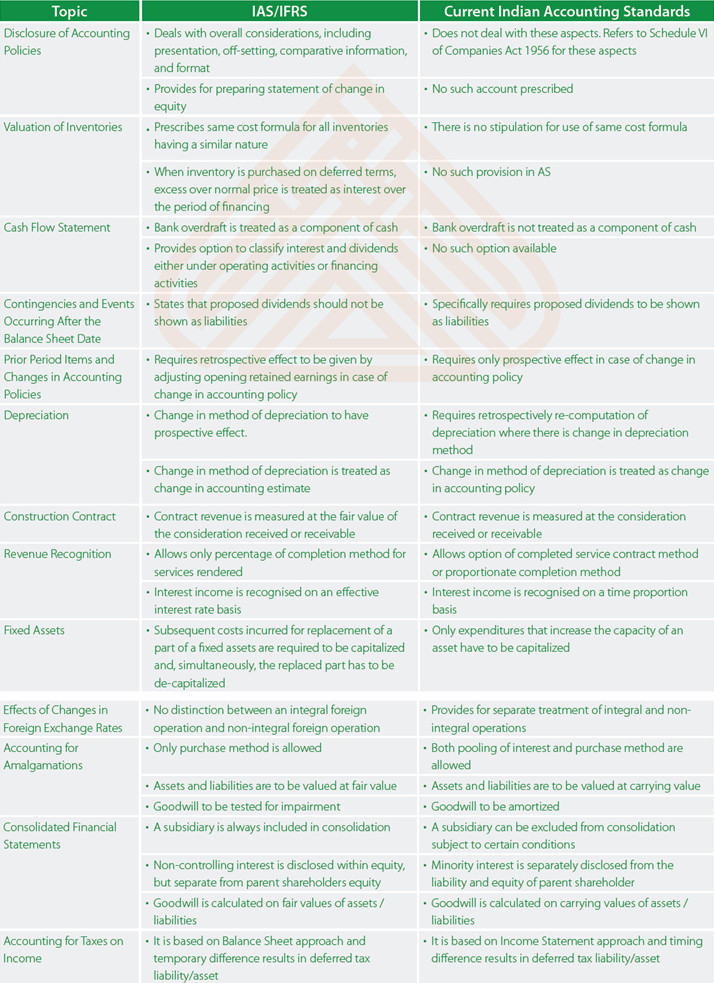

Comparison Of Accounting Standards (2)

Aiming For Global Accounting Standards The International