Best Of The Best Info About Corresponding Figures And Comparative Financial Statements

:max_bytes(150000):strip_icc()/comparative-statement_final-638912a8e4d7465aacd99e115d561f8f.png)

Comparative Statement Definition, Types, And Examples

Sa Information Corresponding Figures And Comparative

Comparative & Commonsize Financial Statements Bizfluent

Comparative Statements Analysis Of Balance Sheet & Quickbooks

Sa 710 Comparative Information Corresponding Figures And

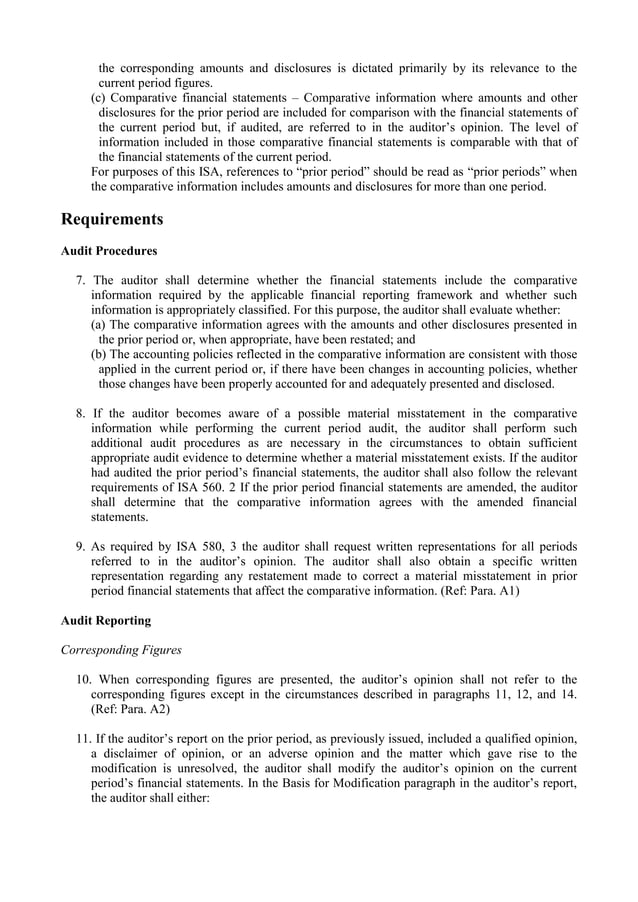

Isa (uk)710 Comparative Information Corresponding Figures And Comp…

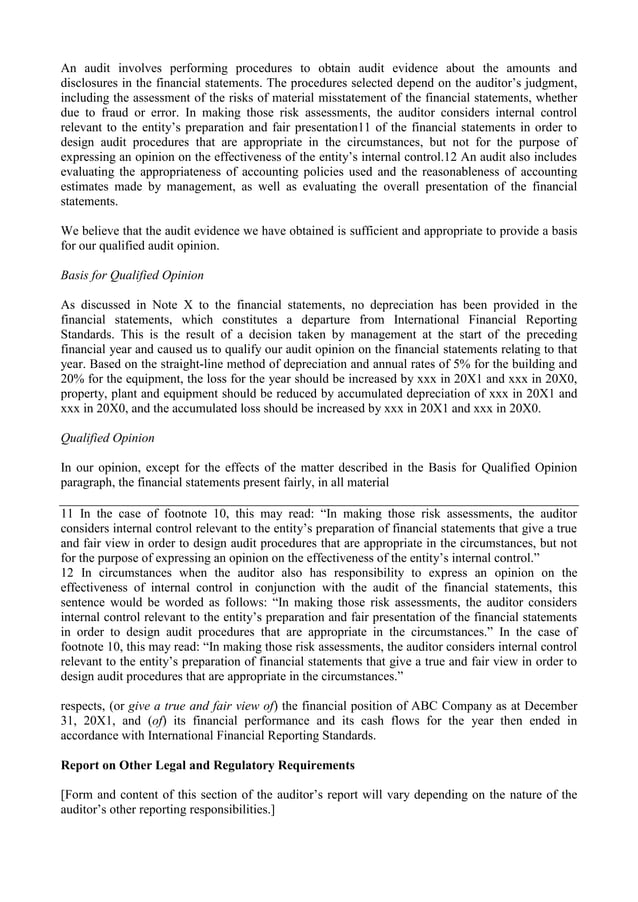

Corresponding figures and comparative financial statements” should be read in conjunction with isa 200 (revised and redrafted), “overall objectives of the.

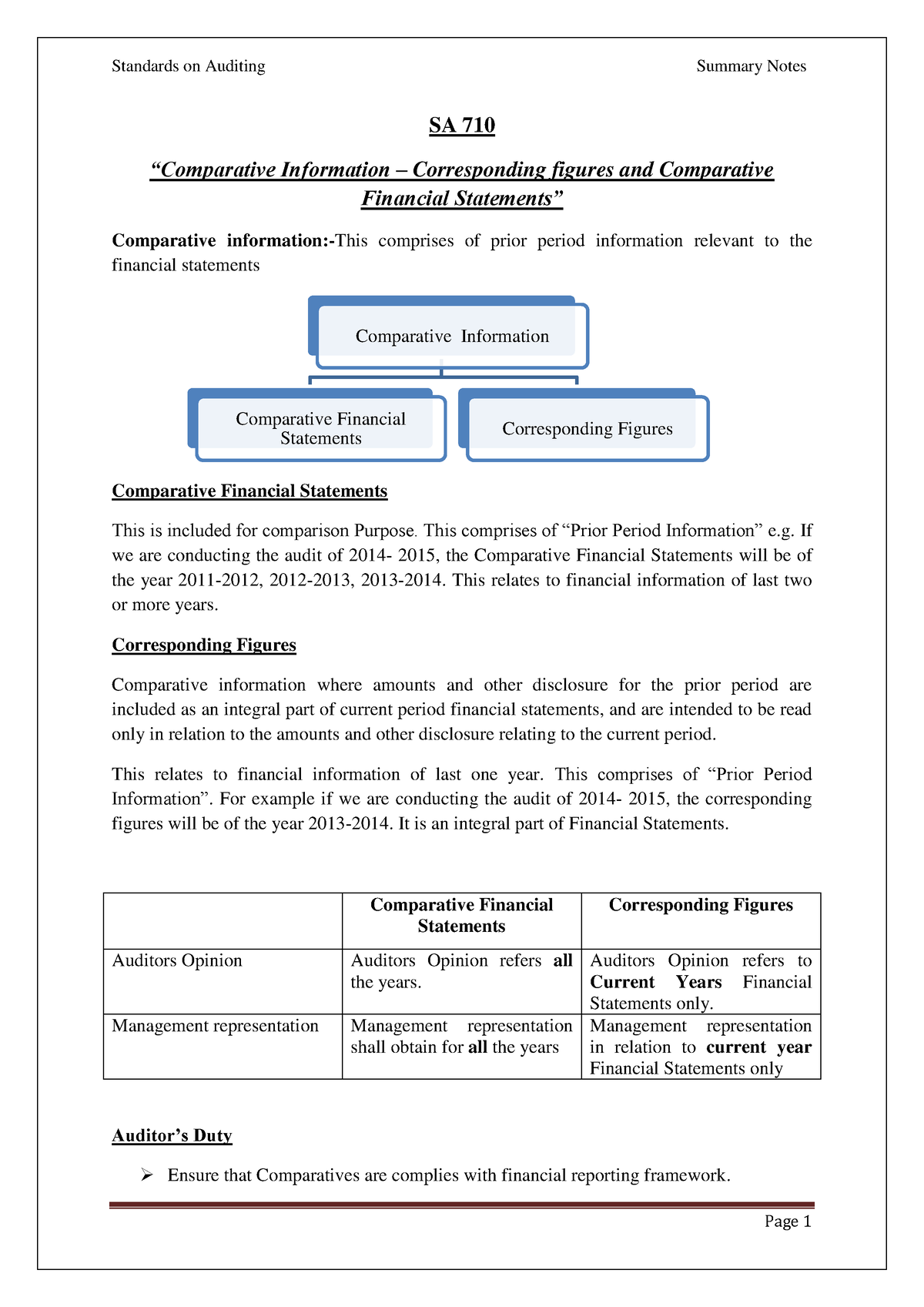

Corresponding figures and comparative financial statements. Corresponding figures where preceding period figures are included as an integral part of the current period financial statements; The essential audit reporting differences between the approaches are: Nov 30, 2008 | basis for.

Caparative figures are categorised into two: Whereas for comparative financial statements, the auditor’s. (a) for corresponding figures, the auditor’s opinion on the financial statements refers to the current period only;

Hong kong standard on auditing (hksa) 710, comparative information—corresponding figures and comparative financial statements, should be read in conjunction with. (a ) for corresponding figures, the auditor’s opinion on the financial statements refers to the. For corresponding figures, the auditor’s opinion on the financial statements refers to the current period only;

(a) for corresponding figures, the auditor’s opinion on the financial statements refers to. Consequently, the format, layout, and paragraph numbering styles. Corresponding figures and comparative financial statements) as the underlying.

For corresponding figures, the auditor’s opinion on the financial statements refers to the current period only; Corresponding figures ‘comparative information’ where amounts and other disclosures for the prior period are included as an integral part of the current period. The comparative financial statements now the comparative.

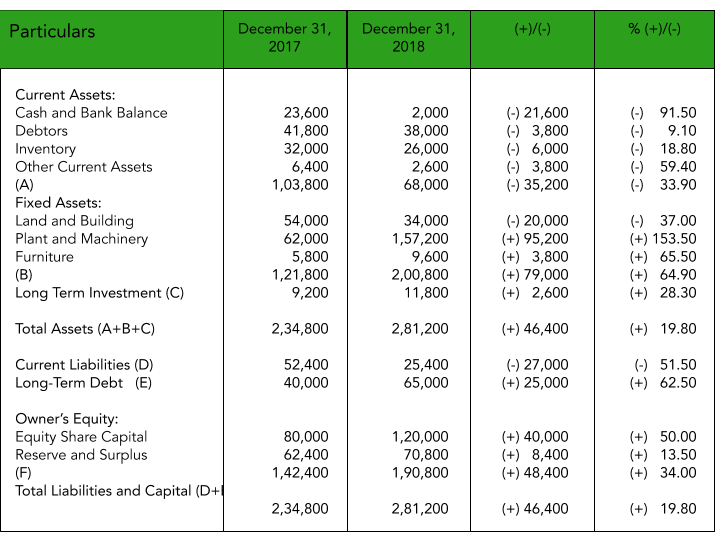

Comparative information represents the amounts and disclosures included in the consolidated annual accounts for one or more previous periods, and provides the users. Isa 710 (redrafted) comparative information — corresponding figures and comparative financial statements. Whereas for comparative financial statements, the auditor’s.

Corresponding figures means “ comparative information where amounts and other disclosures for the prior period are included as an integral part of the current. Whereas (b) for comparative financial statements, the auditor’s opinion refers to each period for Basis for conclusions:

Corresponding figures and comparative financial statements, should be read in conjunction with isa 200, overall objectives of the independent auditor and the conduct.

C\fakepath\isa 710 Comparative Information—corresponding Figures And

Isa (uk)710 Comparative Information Corresponding Figures And Comp…

Comparative Financial Statements, As The Word Suggests, Are

Comparative Financial Statements

Isa (uk)710 Comparative Information Corresponding Figures And

Isa (uk)710 Comparative Information Corresponding Figures And

Reports Arising From Circumstances Addressed In Cas 710, Comparative

Isa (uk)710 Comparative Information Corresponding Figures And Comp…

C\fakepath\isa 710 Comparative Information—corresponding Figures And

Isa (uk)710 Comparative Information Corresponding Figures And Comp…

What Are Comparative Financial Statements? Superfastcpa Cpa Review

Sa 710 Comparative Information Corresponding To Figures &

Corresponding Figures And Comparative Financial Statements Debt Equity