Favorite Tips About Except For Audit Opinion Example

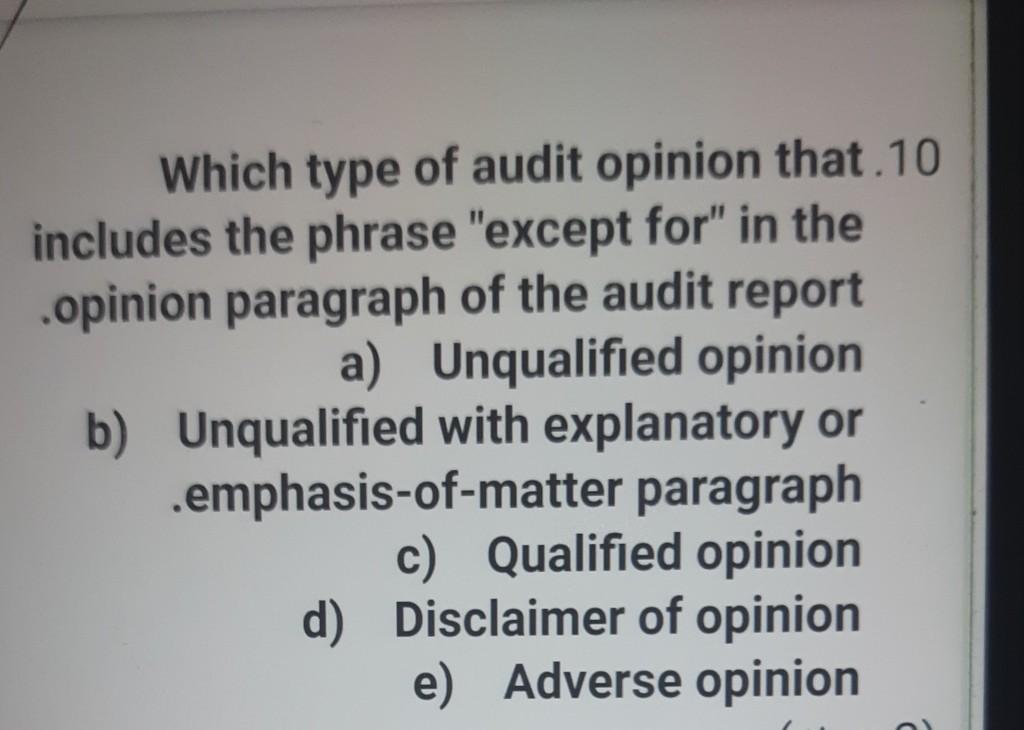

Solved Which Type Of Audit Opinion That.10 Includes The

External Audit

Supplementary Information Audit Opinion Cpa Hall Talk

Audit Report Example Mt Home Arts

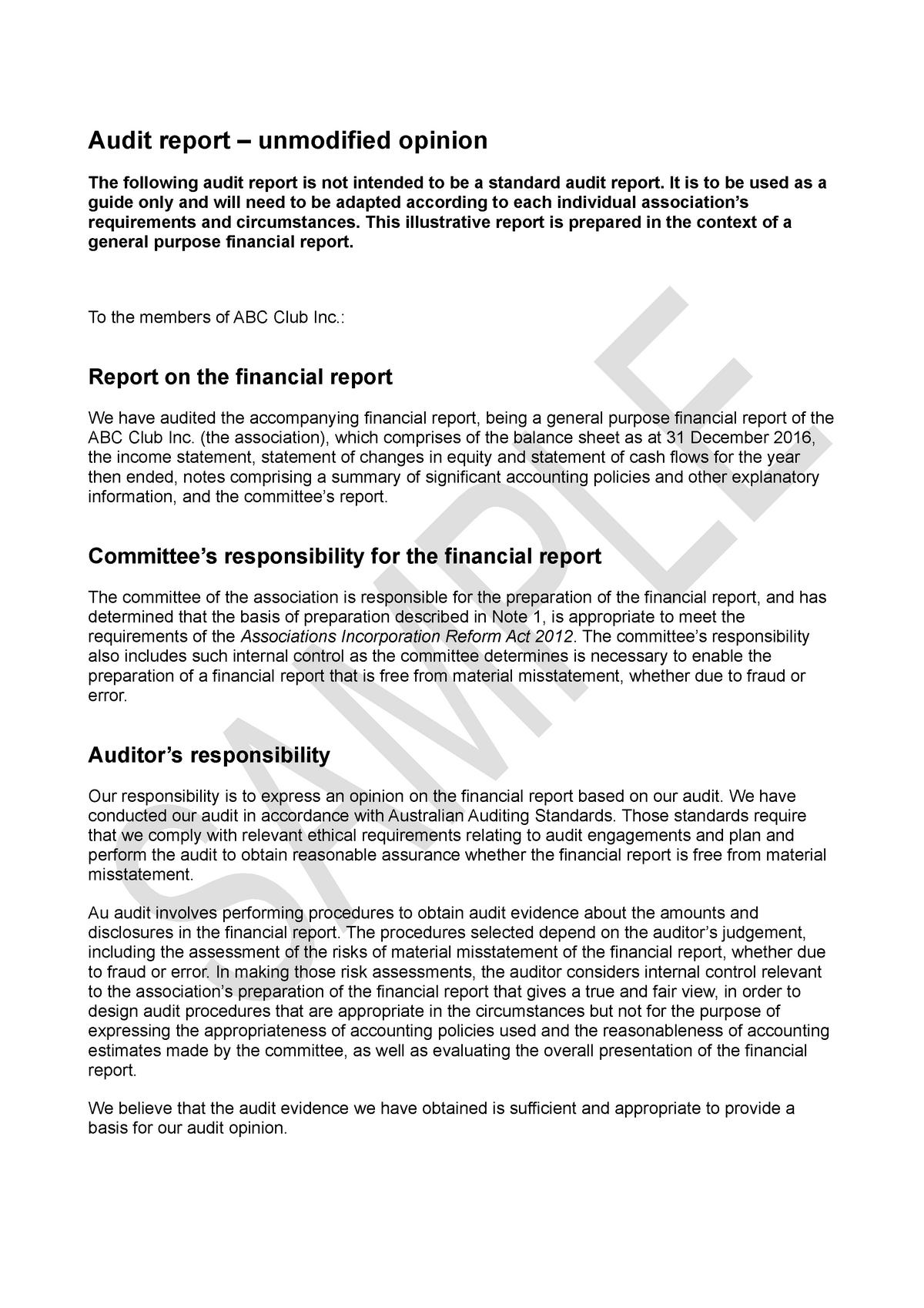

Incorporated Associations Sample Audit Report Unmodified Opinion

Audit Report Qualified Opinion What Is It, Examples

The issue arises when management imposes restrictions or when other conditions occur that make it impossible to engage in certain auditing.

Except for audit opinion example. The auditor shall disclaim an opinion when the auditor is unable to obtain sufficient appropriate audit evidence on which to base the opinion, and the. There are two types of reservations that can be made: The auditor is pricewatercoopers llp (pwc).

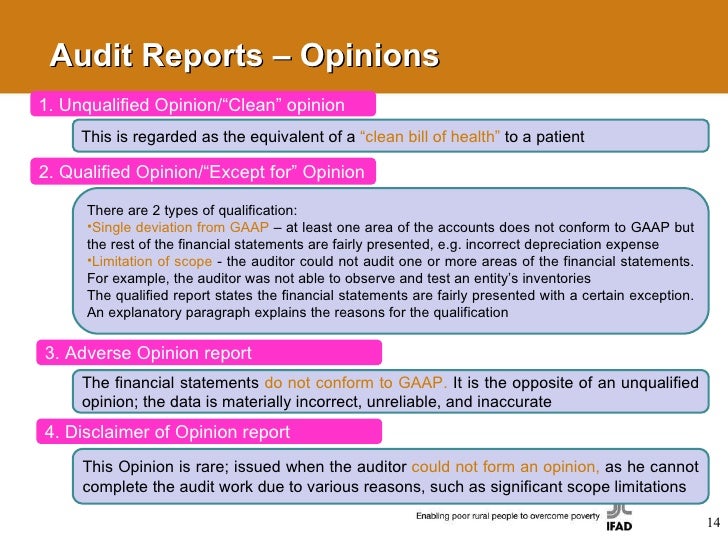

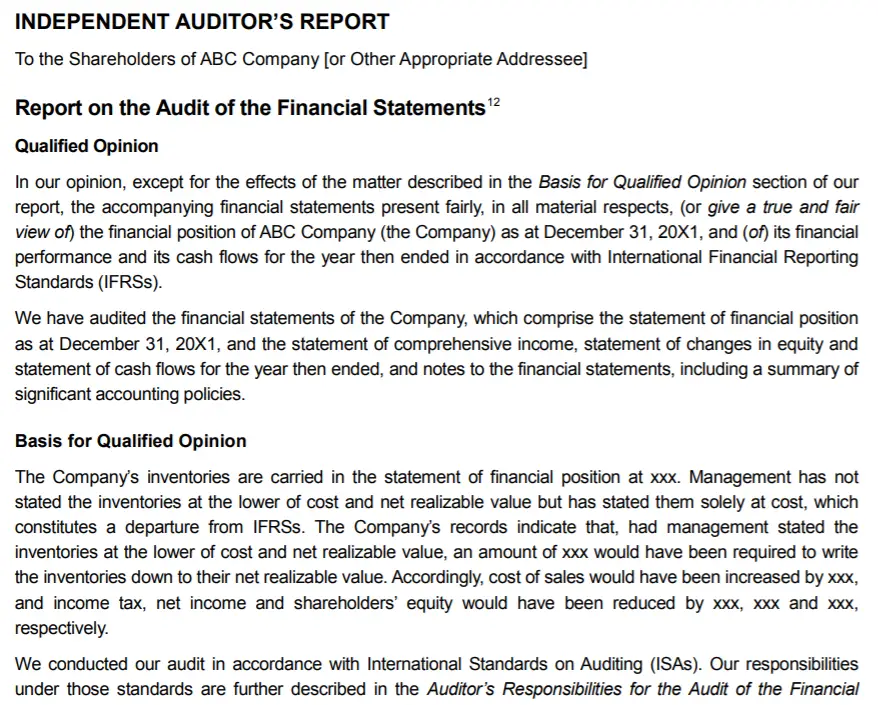

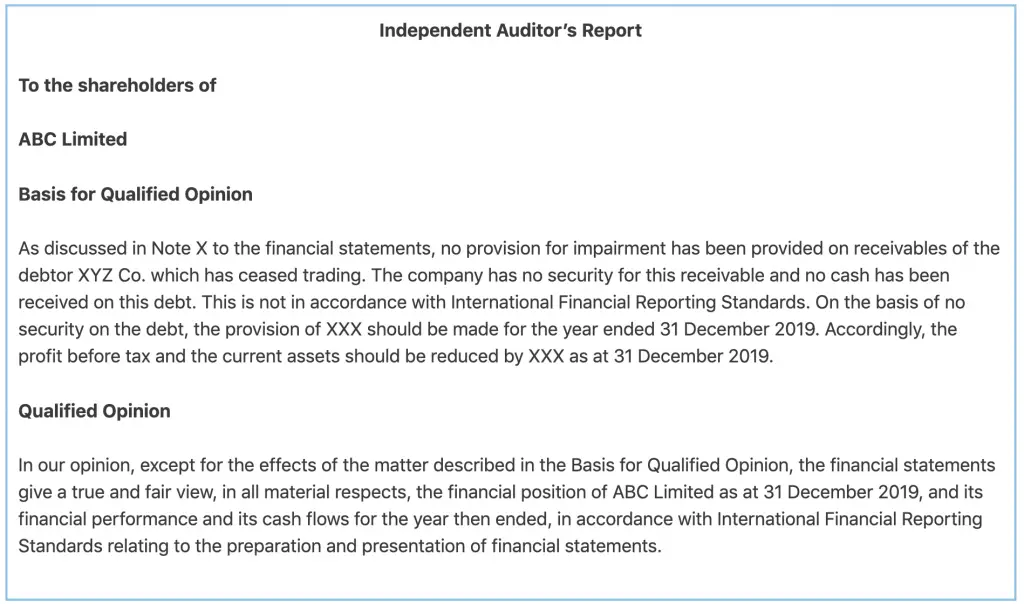

In the independent auditor’s report, an auditor can issue one of five different opinions. Statements, the auditor shall state that, in the auditor’s opinion, except for the effects of the matter(s) described in the basis for qualified opinion section:

Generally, audit opinions are classified into two; Except for the matter described in the basis for qualified opinion section of our report, iin the. If the matter is material but not a fundamental uncertainty or.

Trump’s civil fraud trial as soon as friday, the former president could face hundreds of millions in penalties. Statements, the auditor shall state that, in the auditor's opinion, except for the effects of the matter(s) described in the basis for qualified opinion section: The first section of the.

In our opinion, except for the matter referred to in the. As evident, the auditor issued an. Here is a snapshot of the audit report of tesla inc.

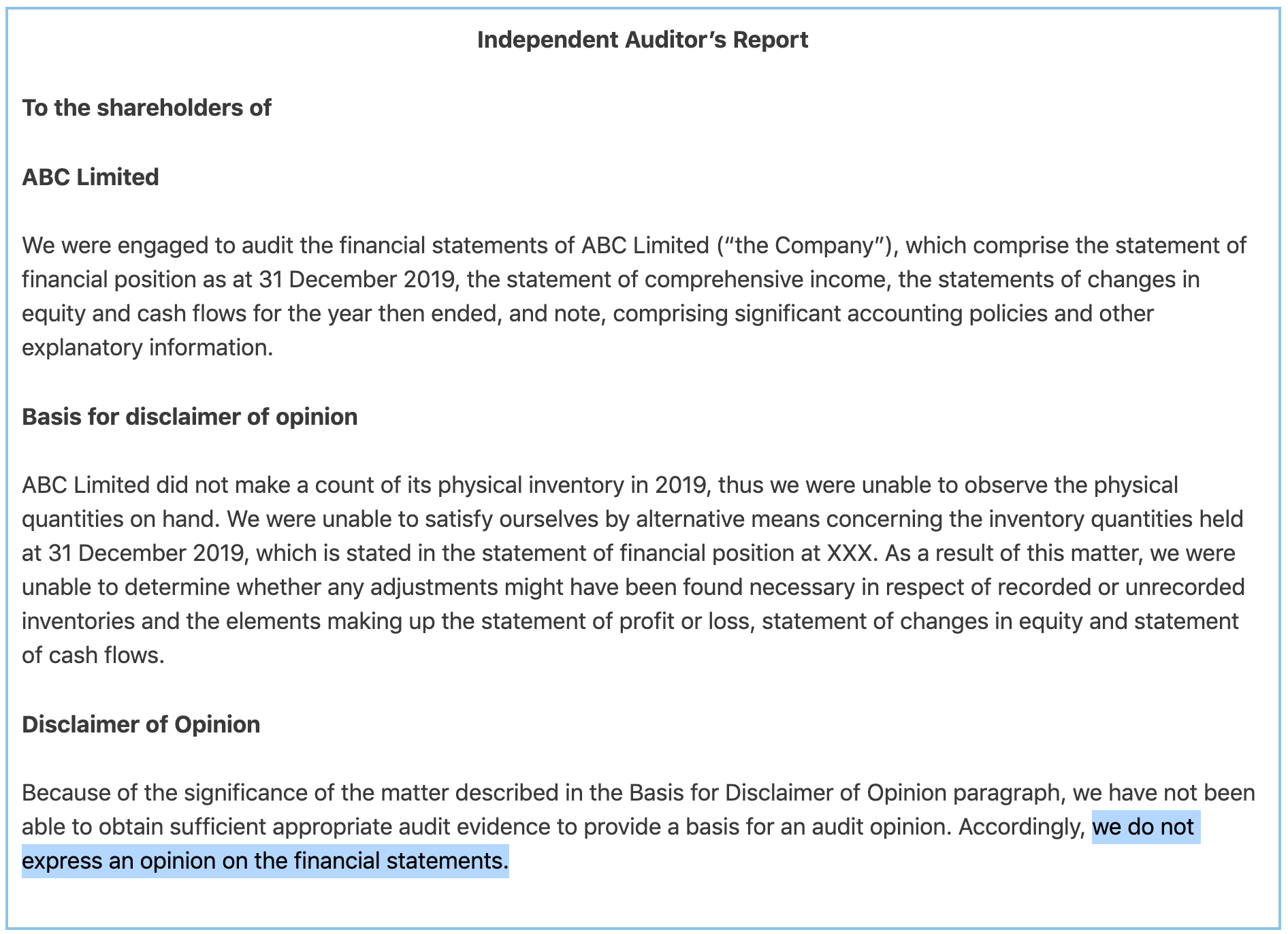

Qualified opinion ('.except for.') adverse opinion ('.do not present fairly.') unable to obtain sufficient appropriate audit evidence: When a new york judge delivers a final ruling in donald j. In this situation the auditor will qualify the audit with an ‘except for’ paragraph i.e.

A gaap departure or a scope. The auditor’s report shall be addressed, as appropriate, based on the circumstances of the engagement. There can be three types of qualified opinions depending upon the circumstances.

Statements, the auditor shall state that, in the auditor’s opinion, except for the effects of the matter(s) described in the basis for qualified opinion section : This paper discusses different audit opinions, including unmodified opinions and other sub.

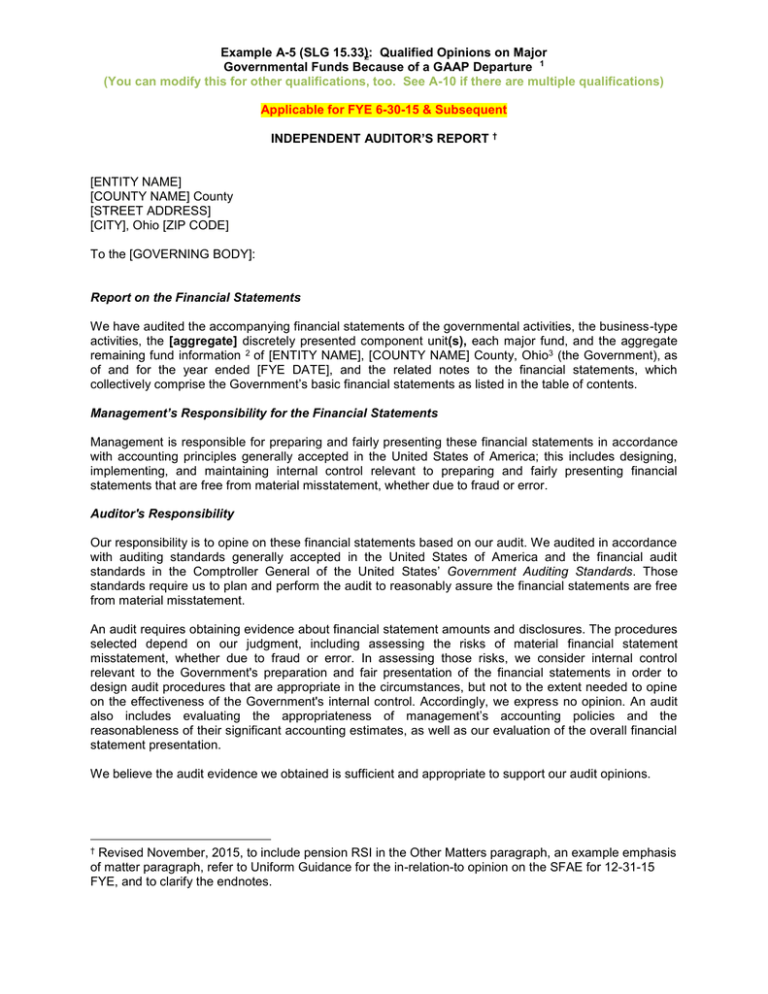

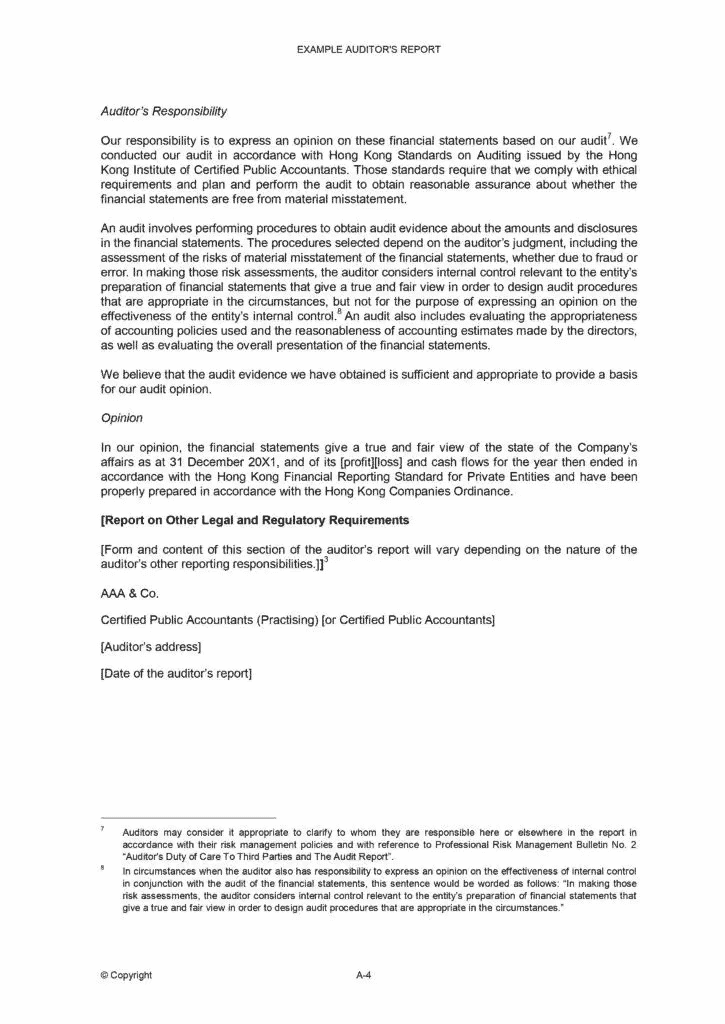

Example A5 (slg 15.33) Qualified Opinions On Major Auditor’s Report

Hong Kong Audit Reports And Opinions Explained Fastlane

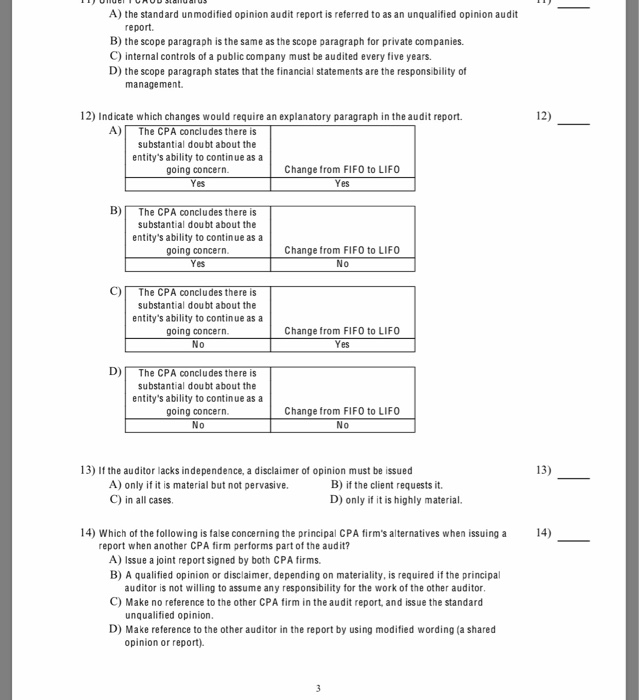

Solved A) The Standard Unmodified Opinion Audit Report Is

What Are Audit Opinions? 4 Types Of Opinions Explained With

Qualified Opinion Definition Example Vs Adverse Accountinguide

Unqualified Vs Qualified Audit Opinion Auditor Report In The 10k

How Write Audit Report To An That Gets Results

What Is An Unqualified Audit Report? Accounting Hub

Supreme Audit Report With Disclaimer Of Opinion Understanding Profit

Audit Opinion Examples Dewsp

Audit Opinion Pdf Auditor's Report Financial

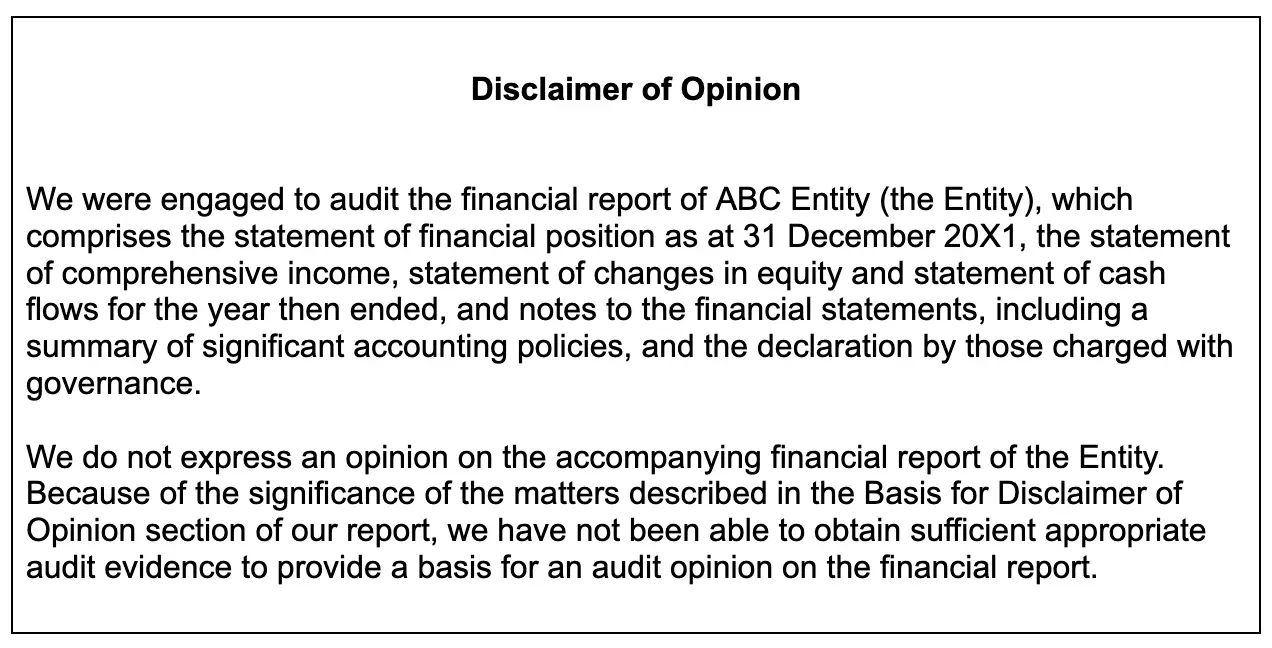

Disclaimer Audit Opinion Example Reasons Accountinginside

Auditor's Report Annual 2020