Fantastic Tips About Preparation Of Trial Balance In Accounting

Sample Trial Balance Sheet Excel My Xxx Hot Girl

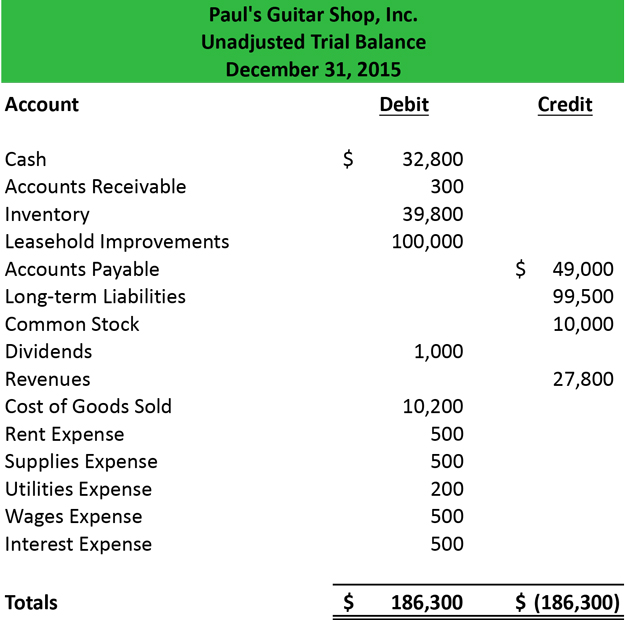

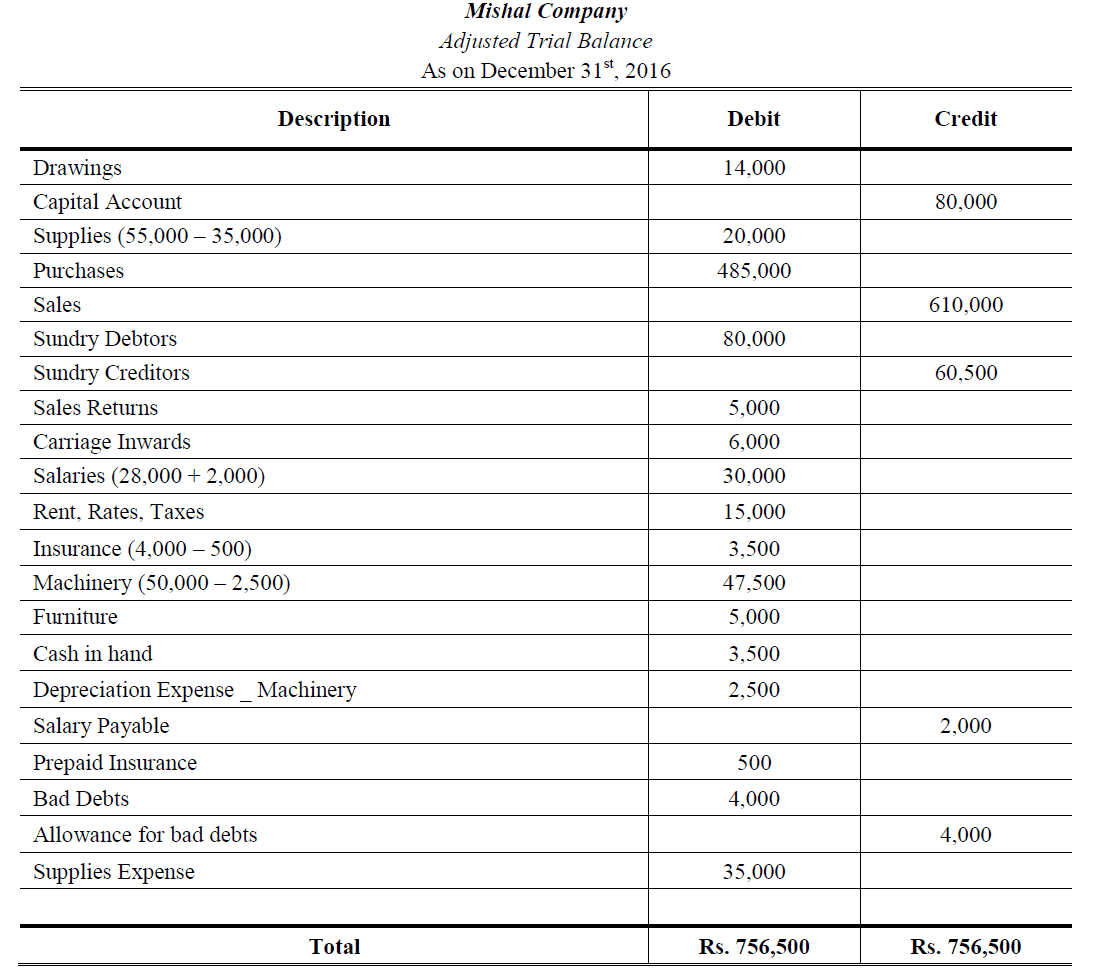

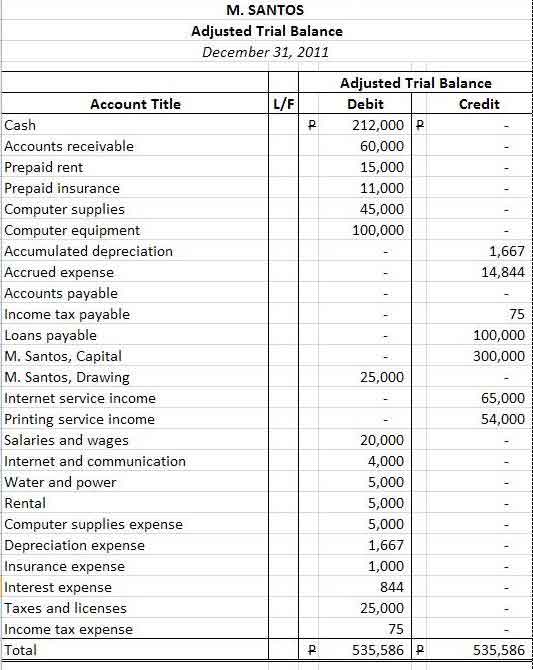

Adjusted Trial Balance Format Examples Questions

:max_bytes(150000):strip_icc()/trial-balance-4187629-1-c243cdac3d7a42979562d59ddd39c77b.jpg)

Trial Balance Definition, How It Works, Purpose, And Requirements

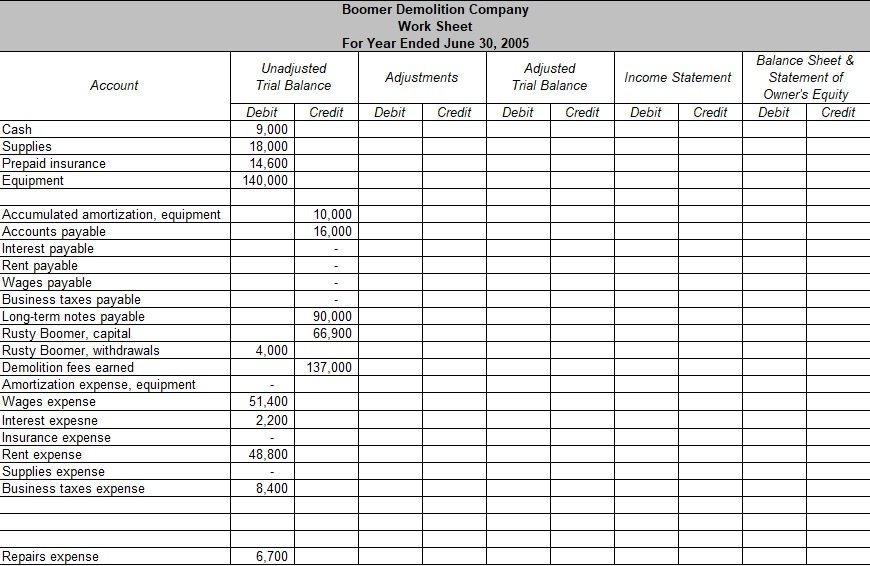

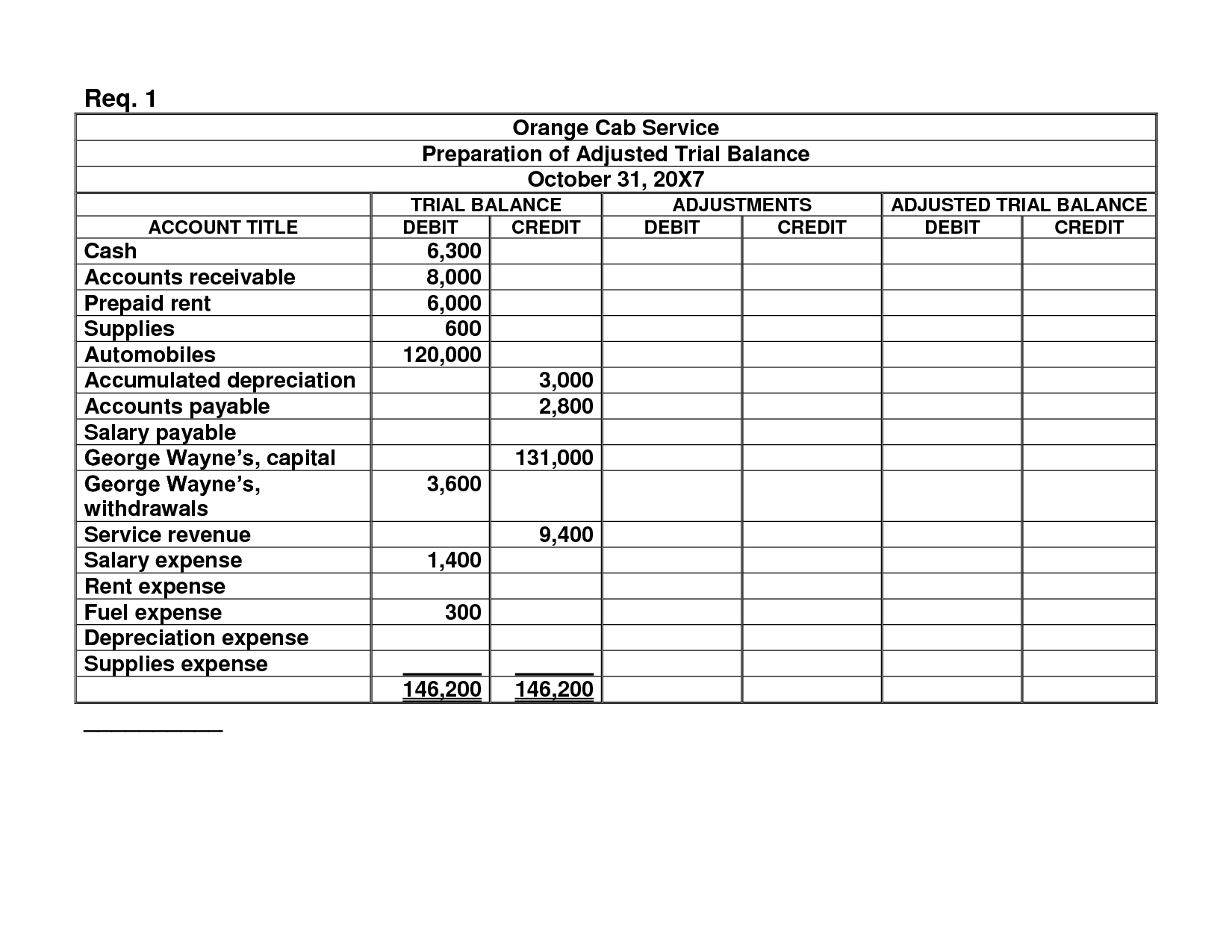

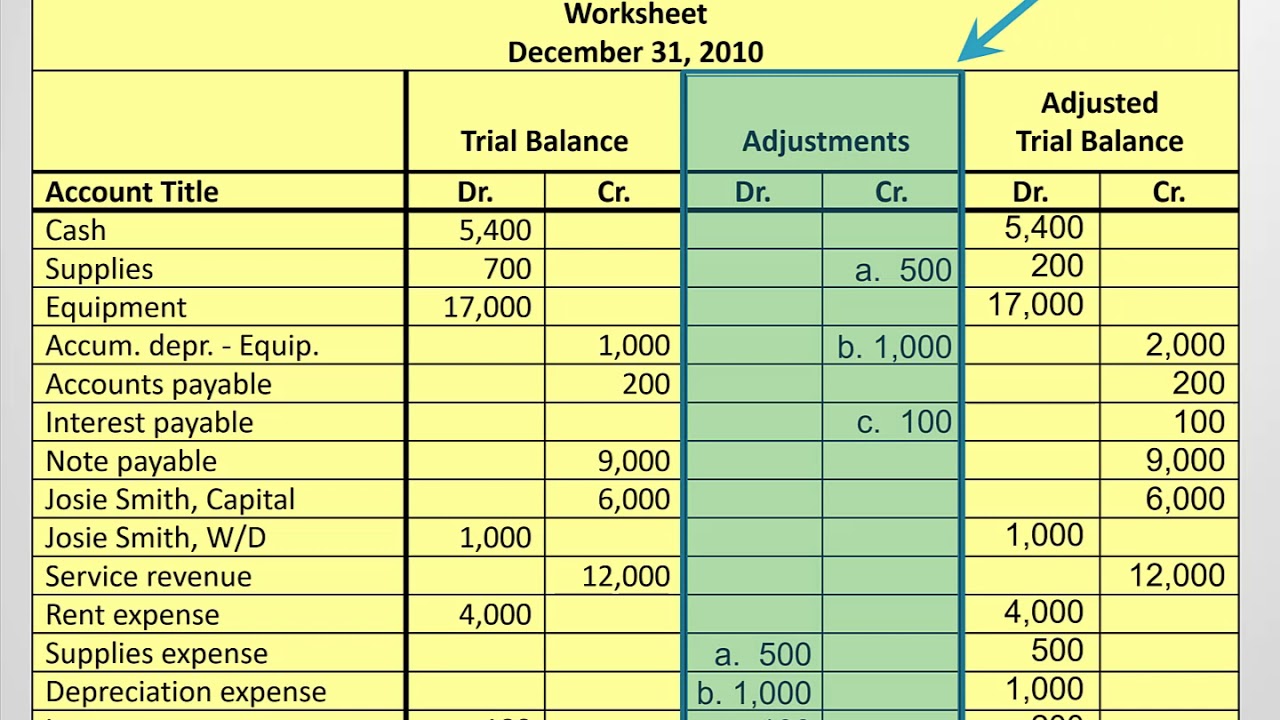

4.5 Prepare Financial Statements Using The Adjusted Trial Balance

Methods Of Trial Balance, Accounting Lecture Sabaq.pk Youtube

Adjusted Trial Balance Format Preparation Examples

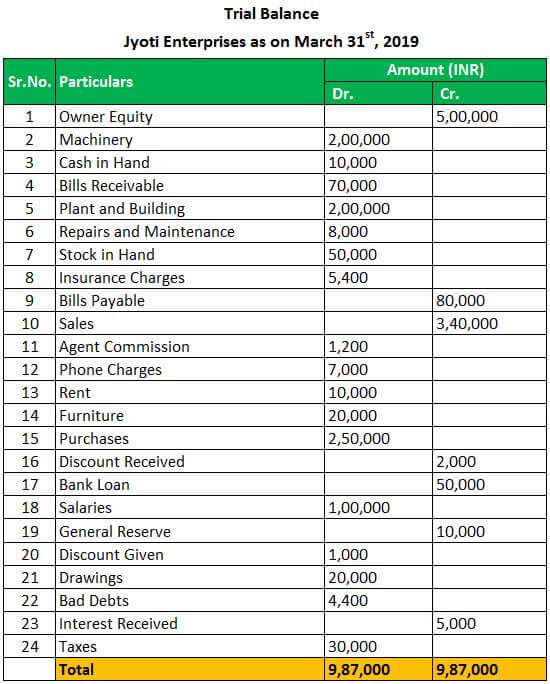

Let’s consider another example to understand the method of preparation of trial balance.

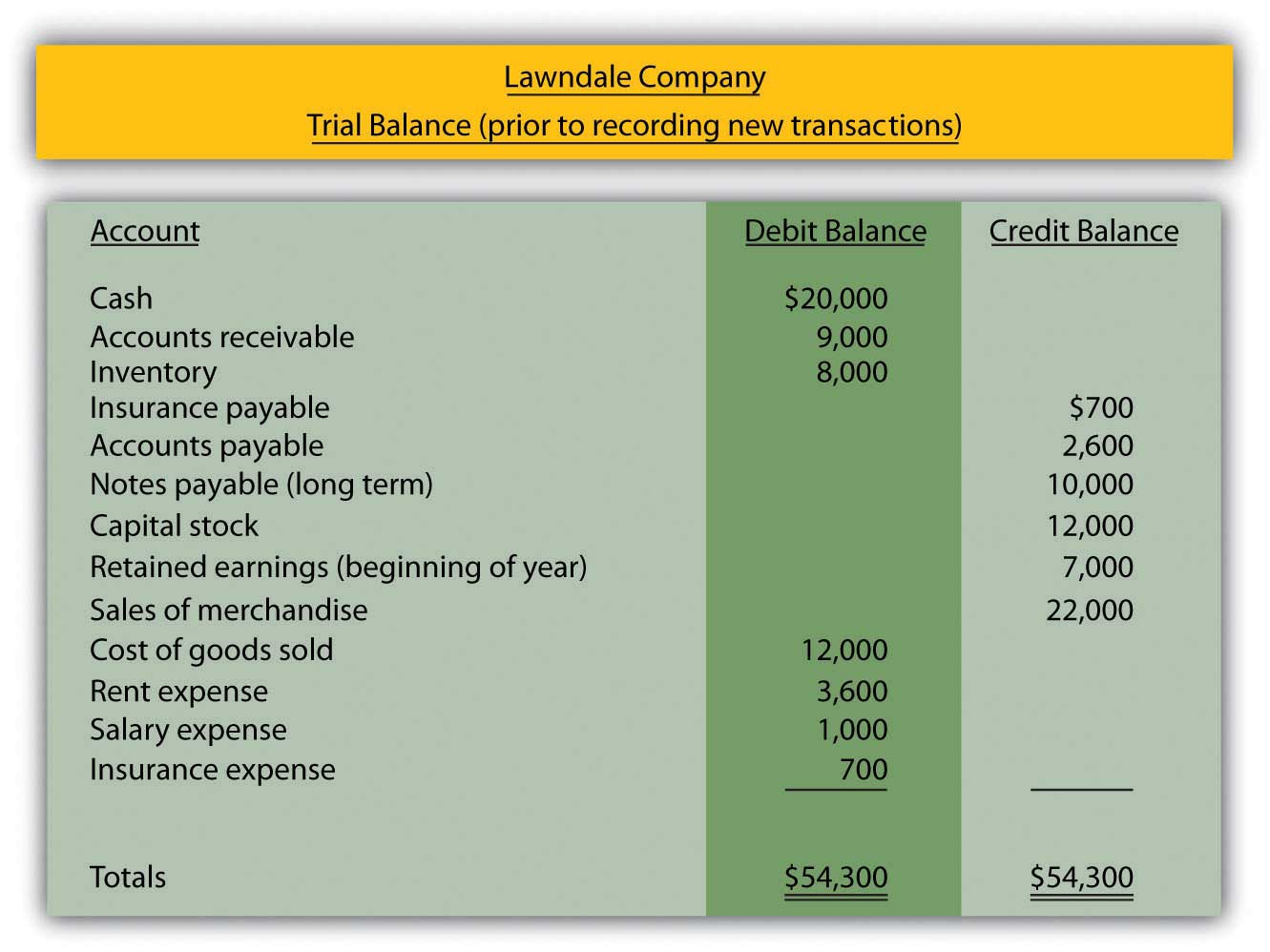

Preparation of trial balance in accounting. Preparing an unadjusted trial balance is the fourth step in the accounting cycle. It includes the columns for account number, account name, debit, and credit balances. Below are the balances from the books of jyoti enterprises as of march 31 st, 2019.

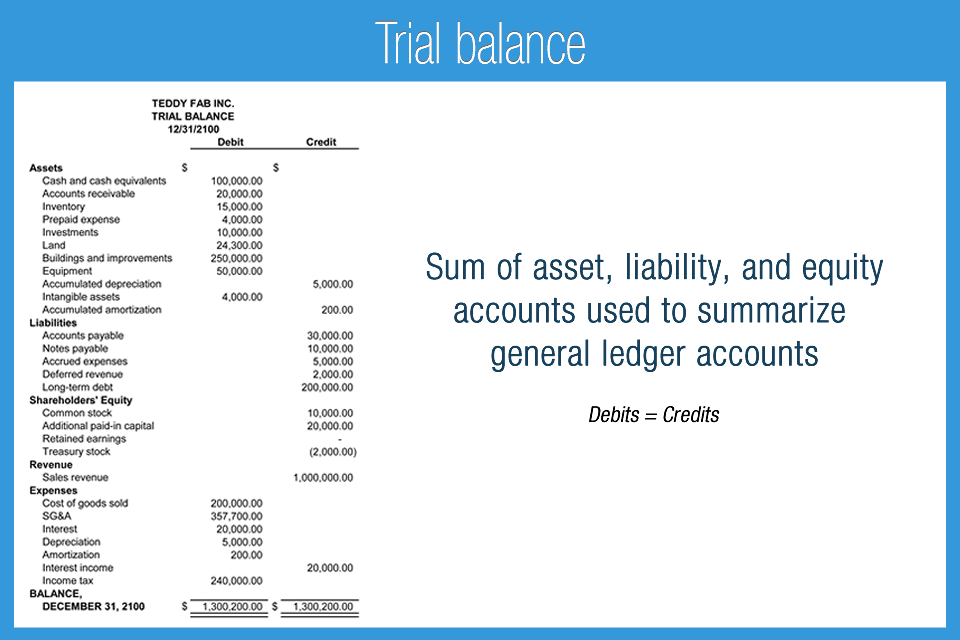

The difference between debit and credit sums gives you the balance. For each open ledger account, total your debits and credits for the accounting period for which you are running the. A trial balance is a list of all accounts in the general ledger that have nonzero balances.

We can prepare the trial balance in the following three ways: Trial balance is cast and errors are identified. A trial balance is a report that lists the balances of all general ledger accounts of a company at a certain point in time.

The main objective of preparing a trial balance is to detect the mathematical accuracy of the ledger balances. Typically, trial balance is prepared at the end of an accounting year. The first step is to make sure that all the ledger accounts are balanced.

Preparing a trial balance for a company serves to detect any mathematical errors that have occurred in the double entry accounting system. The column headers should be for the account number, account name and the. This could be at the end of each month, quarter, half a.

Before you start off with the trial balance, you need to make sure that every ledger account is balanced. To have material for the preparation of the financial statement All ledger accounts are closed at the end of an accounting period.

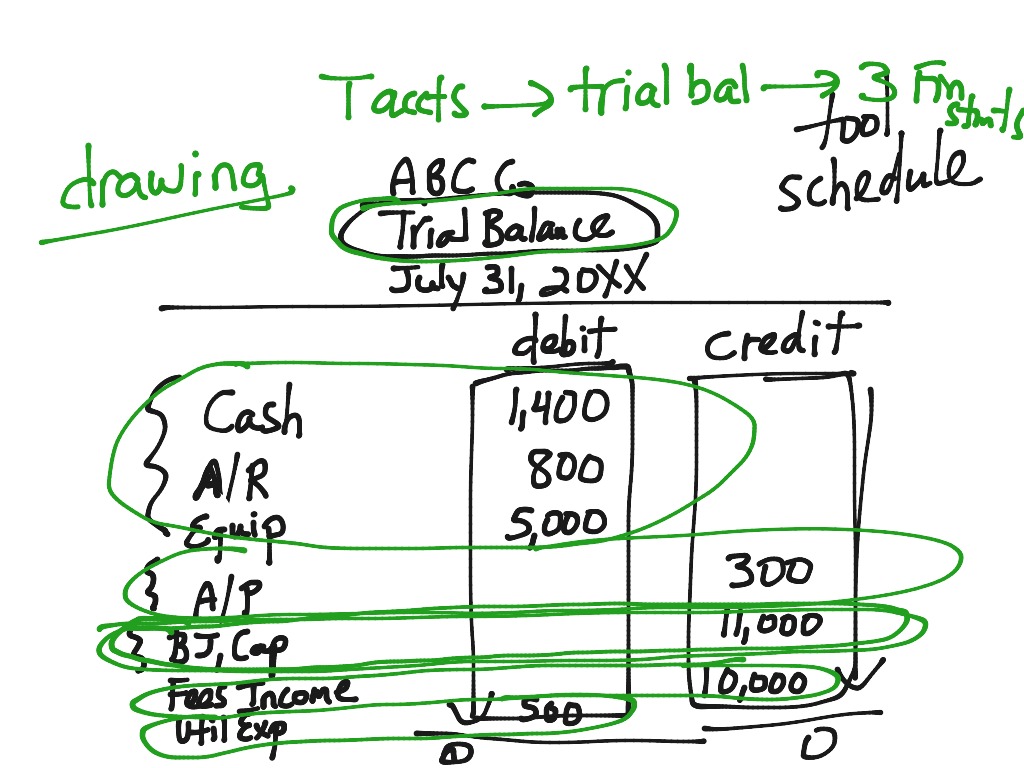

Following steps are involved in the preparation of a trial balance: Creating a trial balance in accounting represents a pivotal step within the broader financial reporting process. It is usually prepared at the end of an accounting period to assist in the drafting of financial statements.

How do you prepare a trial balance? When the accounting system creates the initial report, it is considered an unadjusted trial balance because no adjustments have been made to the chart of accounts. It’s used at the end of an accounting period to ensure that the entries in a company’s accounting system are mathematically correct.

To have balances of all the accounts of the ledger to avoid the necessity of going through the pages of the ledger to find it out. The accounts reflected on a trial balance are related to all major accounting items, including assets, liabilities, equity, revenues, expenses, gains, and. There are various objectives for preparing trial balance which is mentioned below:

Preparation of trial balance is the third step in the accounting process. A trial balance ensures mathematical accuracy in a company’s financial records by presenting a snapshot of debits and credits for a specific period. The preparation of a trial balance helps consolidate, verify, and rectify journal entries, shaping tax returns and audit reports.

Adjusted Trial Balance Definition, Preparation & Example Video

Adjusted Trial Balance Template Excel

Trial Balance Accounting Play

Ppt List The Steps In Accounting Cycle Powerpoint Presentation

Trial Balance Definition And Examples Of Images

Trial Balance Accounting Showme

Accounting Trial Balance Example And Financial Statement Preparation

Wonderful Balance Sheet Accounts Are Not Affected By Adjustments Profit

Trial Balance Examples Real Life Example Of In Accounting

How Does An Organization Accumulate And Organize The Information

Accounts Preparationtrial Balance & Etb Cut Out Activity Teaching

How To Make A Statement Of Changes In Owner's Equity Business Tips

What Is The Adjusted Trial Balance And How It Created? Youtube