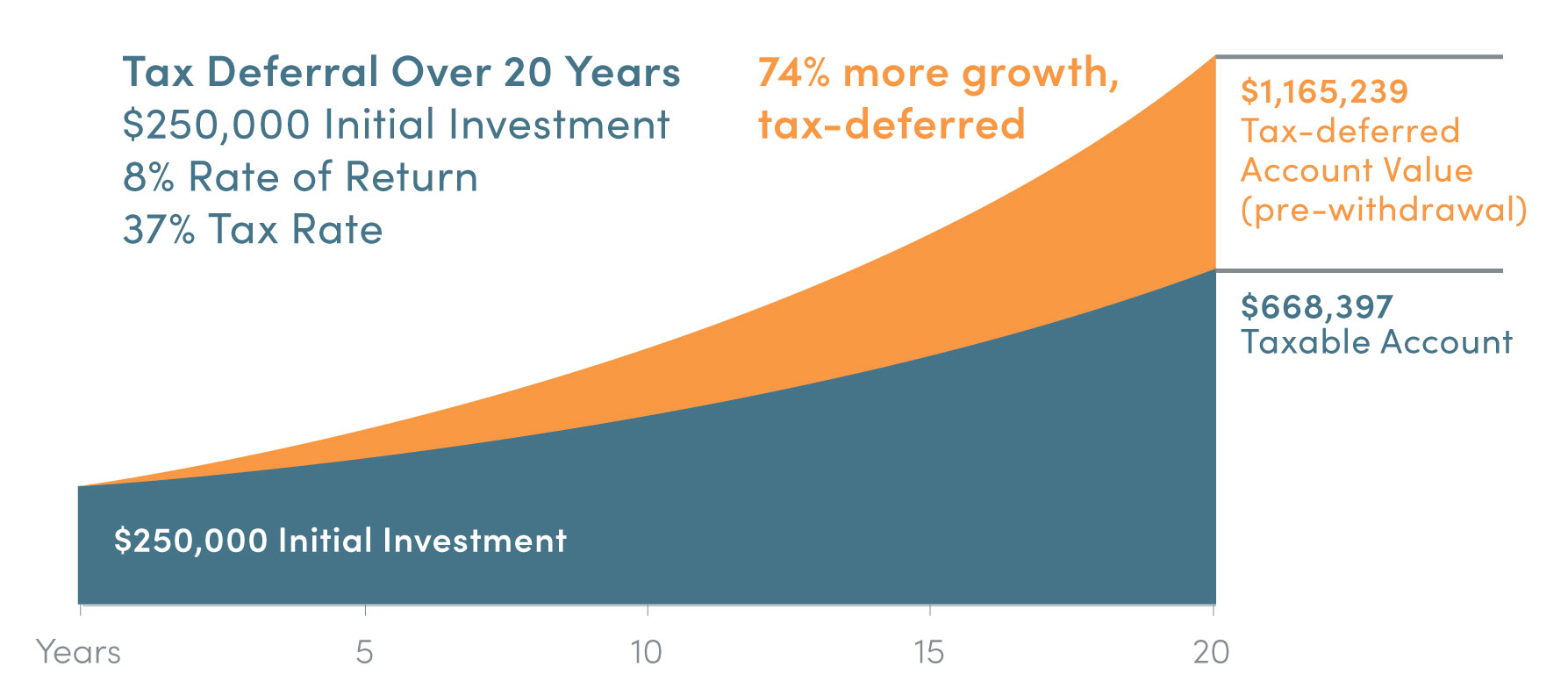

Unique Info About Aggregate Cash Flow Tax Deferred Examples

Deferred Tax Liabilities Explained (with Reallife Example In A

What Does Statement Of Cash Flows Mean In Business? The Mumpreneur Show

Discovermumu Blog

[solved] Edgar Detoya, Tax Consultant, Began His Practice On Dec. 1

![[Solved] Edgar Detoya, tax consultant, began his practice on Dec. 1](https://einvestingforbeginners.com/wp-content/uploads/2020/09/ctsh3.png)

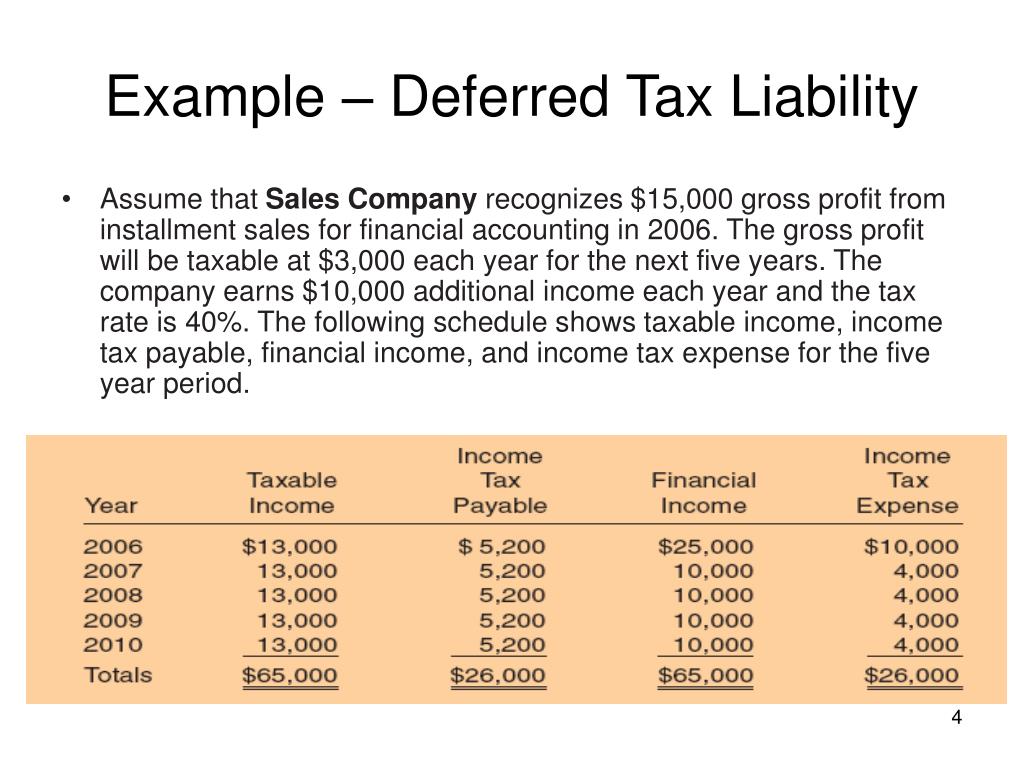

Below is an example scenario in which a deferred tax liability is created.

Aggregate cash flow tax deferred examples. Net income = $1,365,000. Yet, the estimated magnitude of these implied cash flows is rather small. Under this approach, deferred tax is recognised on timing differences between accounting profit and taxable profit, hence the focus of the timing difference approach is on the profit.

The objective of ias 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by means of a statement of. The applicable effective tax rate was 30%. Common types of deferred taxes.

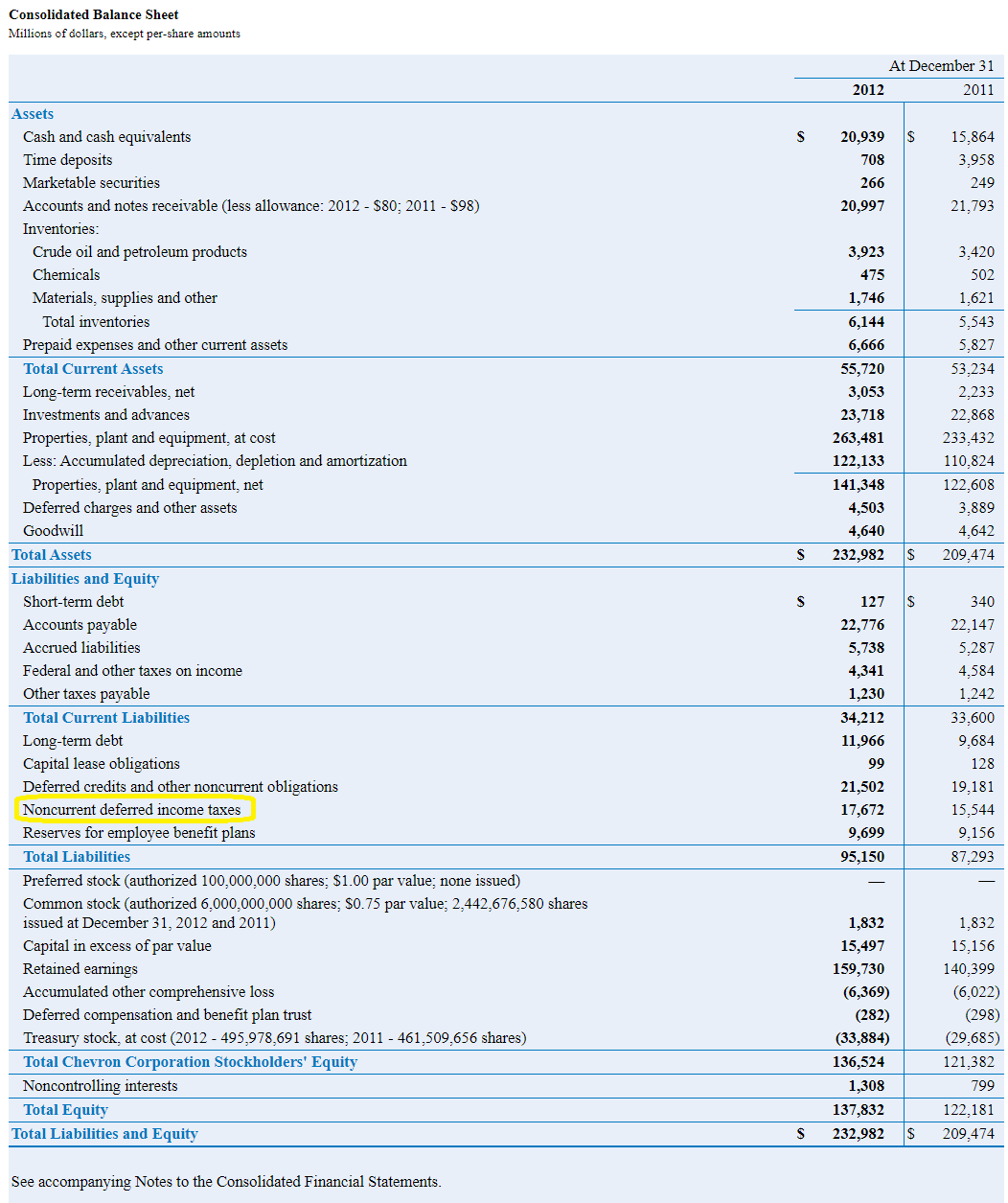

Deferred tax liabilities are generally recognised for all temporary differences that will result in taxable amounts in determining taxable profit (tax loss) of future periods. We explain how to calculate deferred tax expense and rates along with step by step calculations. In the same of 2017, the deductible difference between.

However, as it is not an. Had a trade receivable balance equivalent to $10,000 and $15,000 at the end of 2017 and 2018 respectively. Depreciation the most notable creation of a deferred tax liability is due to differences between how depreciation is calculated by an appropriate.

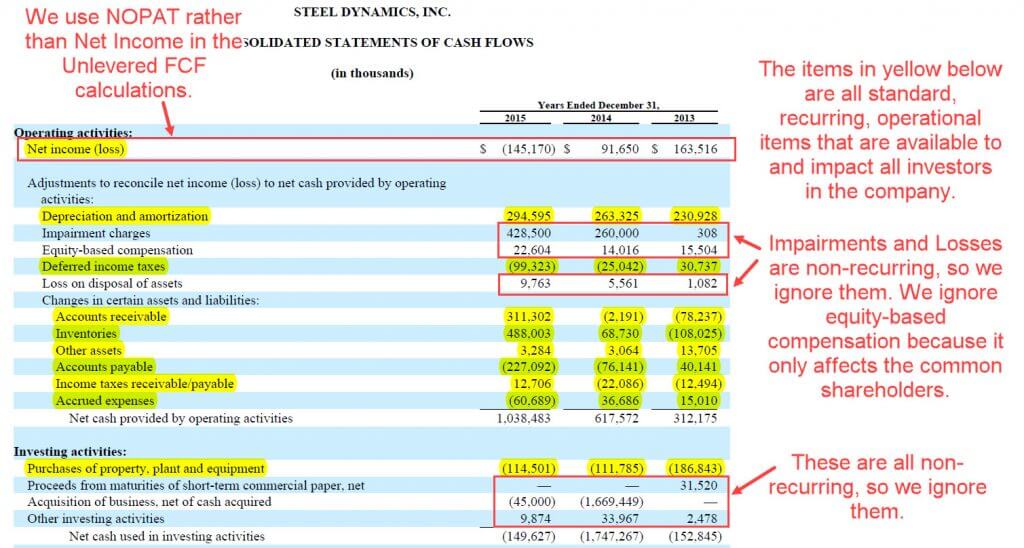

2010 deferred tax liability = 40. If we prepare a statement of cash flow using the direct method, the deferred tax will not show in operating activities as it is not a cash. Examples of items that give rise to the recognition of deferred taxes includes:

07/01/2012) i'm forecasting cash flow for a company that has a dtl and nols. If a business incurs a loss in a financial year, it usually is entitled to use that loss. Deferred tax on statement of cash flow.

Fact pattern company buys a $30 piece of equipment (pp&e) useful life of 3 years for book. Depreciation is an expense that acts as a tax shield. Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability of the entity to generate cash and.

As 3 cash flow statements states that cash flows should exclude the movements between items which forms part of cash or cash equivalents as these are. Deferral accounts, ias 26 accounting and reporting by retirement benefit plans, ias 27 separate financial statements,. Let’s take 3 examples of that:

Cfat = $1,365,000 + $180,000. One straightforward example of a deferred tax asset is the carryover of losses. Deferred tax liability example:

This article has been a guide to what is deferred tax & its meaning. The tax base used for computing tax was equivalent to $12,000 in 2017, and $10,000 in 2018.

Does Deferred Revenue Go On The Cash Flow Statement? Your Business

Deferred Tax (dit) Definition, Types And Examples Marketing91

Ppt Deferred Tax Examples Powerpoint Presentation, Free Download Id

Deferred Revenue Debit Or Credit And Its Flow Through The Financials

How To Record Saas Deferred Revenue? Freecashflow.io

How Gst Deferrals Will Benefit Your Cash Flow When Importing Into

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset What It Is And How To Calculate Use It, With

Bookkeeping To Trial Balance Example Of Deferred Tax Liability

Deferred Tax Demystified

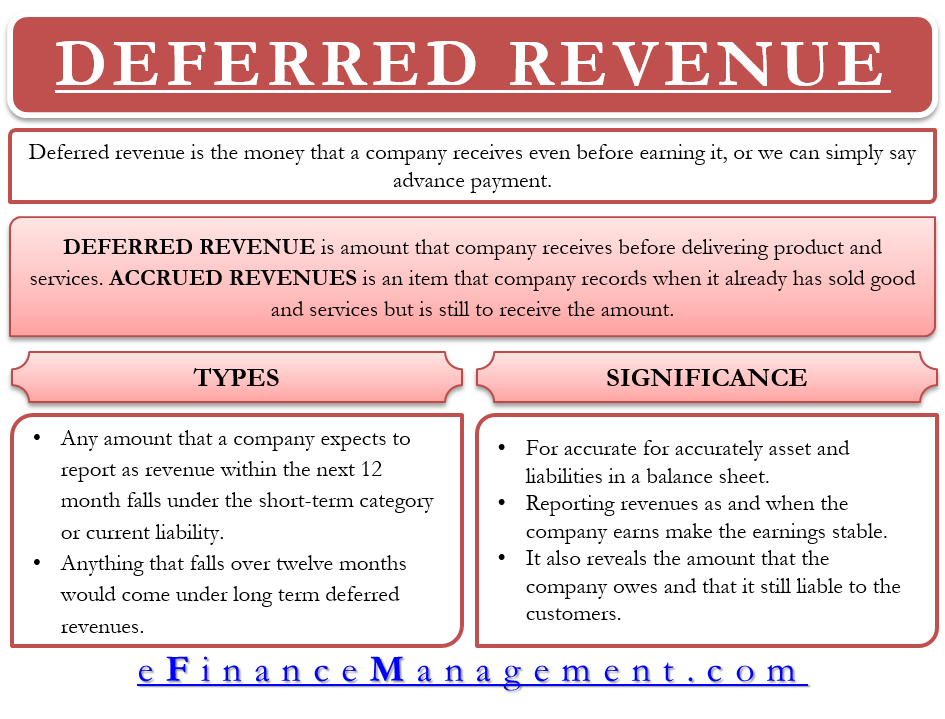

Deferred Revenue Meaning, Importance And More

:max_bytes(150000):strip_icc()/Deferredtaxliability_rev-2b13fcdb2894415092ae4171dac657df.jpg)

:max_bytes(150000):strip_icc()/TermDefinitions_DeferredTax_V2-d5ae6ed922204f7eaa8bfb6b7b4b7f44.jpg)

Deferred Tax Asset Calculation, Uses, And Examples