Marvelous Info About Statement Of Standard Accounting Practice

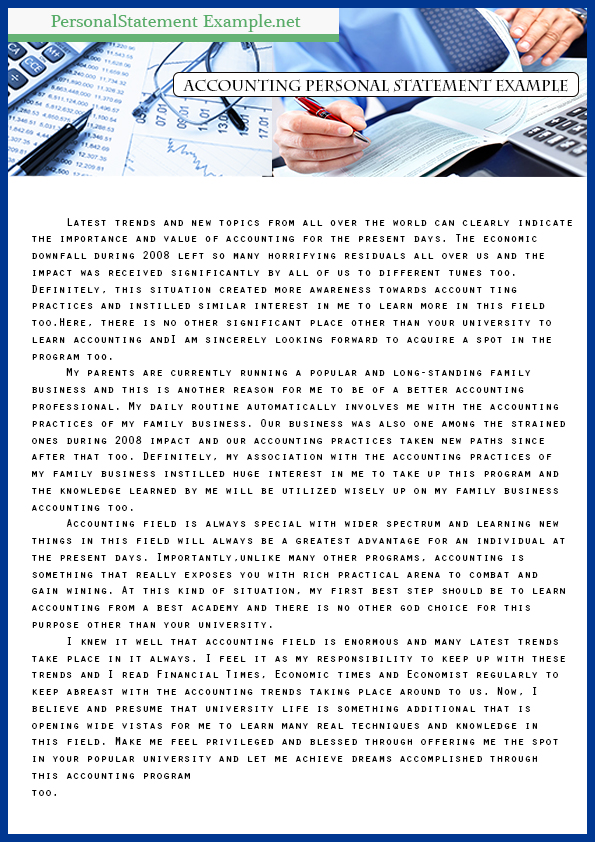

Best Made Personal Statement Accounting Example

Solution Financial Accounting Practice Exam Studypool

What Are Accounting Standards List Of In Detail

Ppt Lesson 34 Powerpoint Presentation, Free Download Id5915898

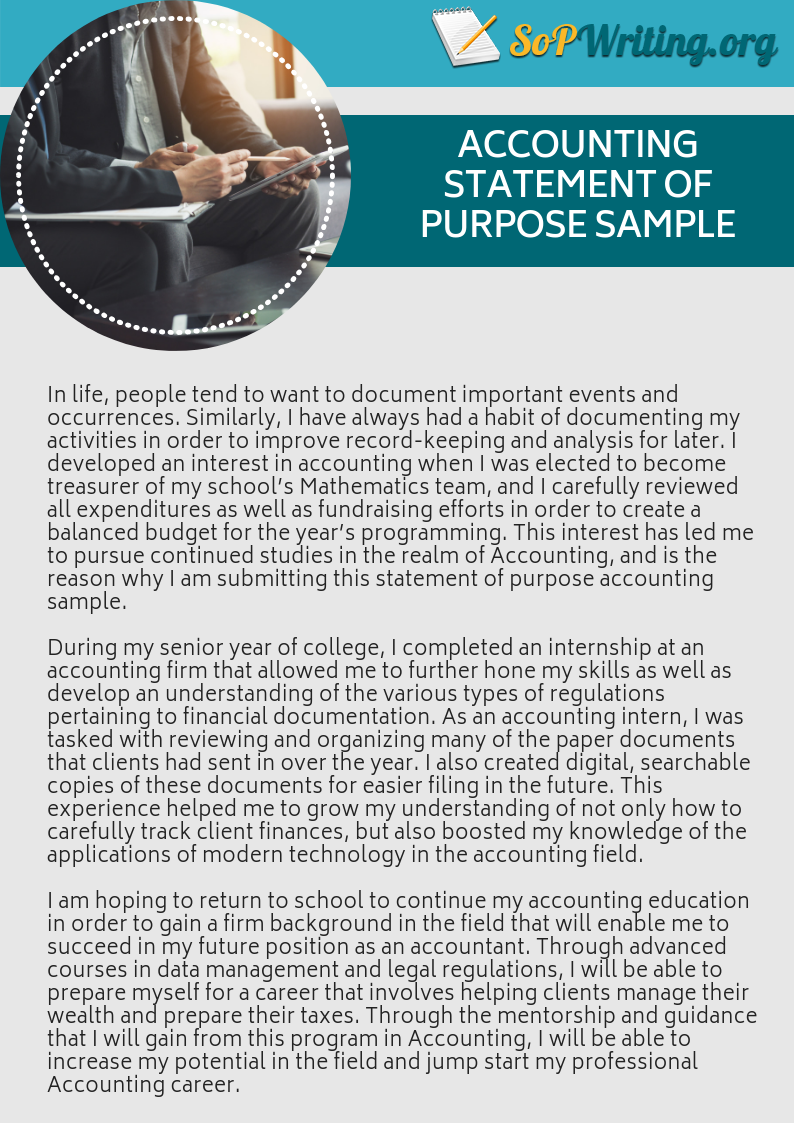

Impress With Your Sop Accounting Admissions

Financial Statement

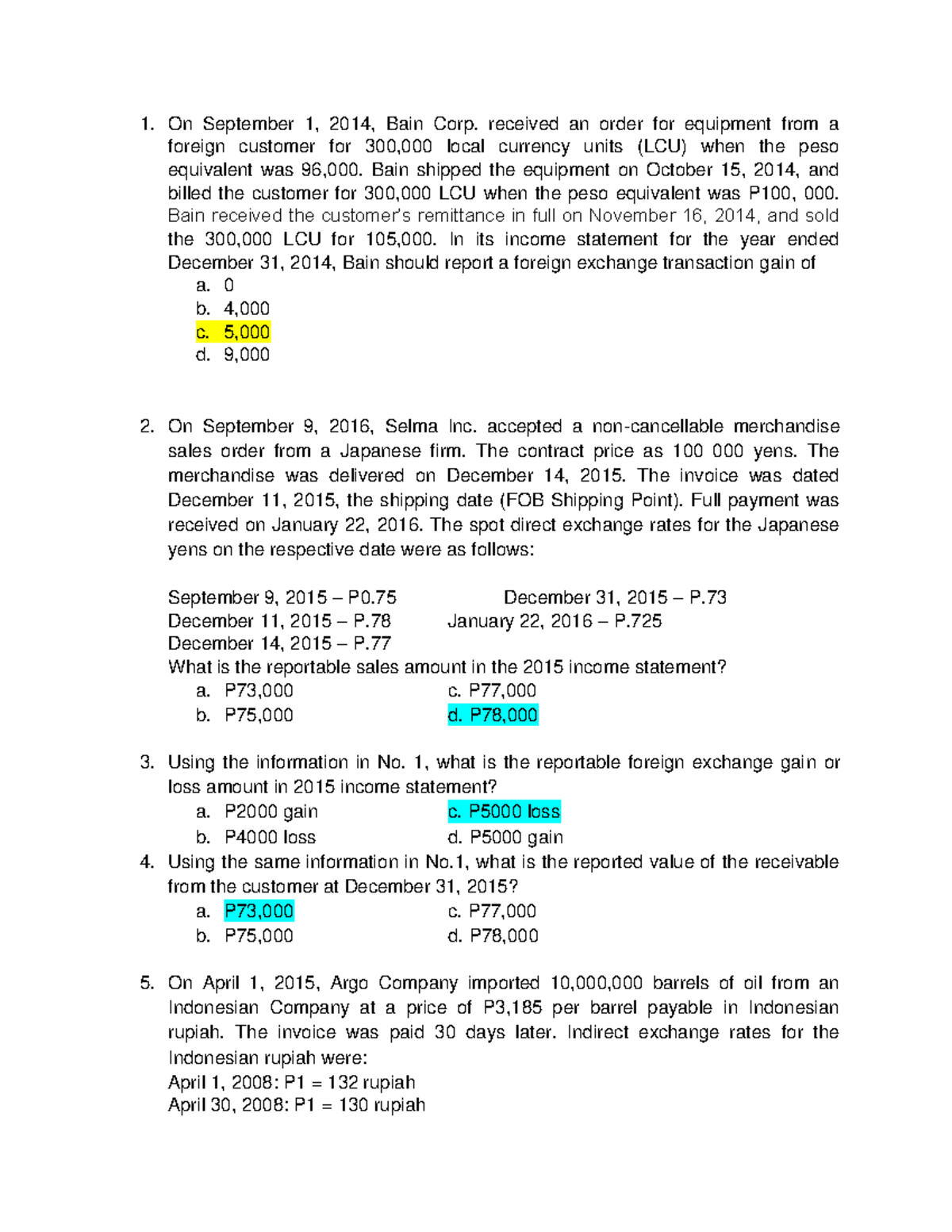

Proforma methods of accounting treatments (cf.

Statement of standard accounting practice. Statement of standard accounting practice by institute of chartered accountants in england and wales., 1978, institute of chartered accountants in england and wales edition, in english. Statements of standard accounting practice abstract. A total of 34 statements (or revised statements) went on to be released between 1971.

Statements of standard accounting practice are not intended to apply to immaterial items (see paragraph 8 of the foreword). The practices set out in this statement should be regarded as standard in respect of financial statements relating to periods beginning on or after 1 october 1997. Earlier adoption is encouraged but not required.

The need for materiality judgements is pervasive in. See also financial reporting standard; Objective the objective of this statement is to prescribe the basis for presentation of general purpose financial statements, in order to ensure comparability both with the enterprise's own financial statements of previous periods and with the financial.

Statements of standard accounting practice (ssaps) by the major accountancy bodies. Except for paragraph 1, the accounting practices set out in this statement should be adopted as soon as possible and regarded as standard in respect of financial statements relating to periods ending on or after 31 october 1994. Scope this statement shall be applied to the primary financial statements, including the consolidated financial statements, of any.

(practice statement) provides companies with guidance on how to make materiality judgements when preparing their general purpose financial statements in accordance with ifrs standards. Generally superseded by financial reporting standards. While some of the ssaps have been superseded by financial reporting standards (frs), some remain in.

Where, for various reasons, this uniformity. Ssap, or statements of standard accounting practice, are edicts by which trading companies that are listed on the stock market must adhere to when constructing their financial reports. Statement of standard accounting practice published on by oxford university press.

View the related practice notes about. Statements of standard accounting practice were issued by the accounting standards board and although many have been superseded by financial reporting standards, some are still in force for accounting. The accounting practices set out in this statement should be regarded as standard in respect of financial statements relating to periods beginning on or after 1 january 2001.

These accounts have been prepared in accordance with all. The first statement of standard accounting practice (ssap), on 'accounting for the results of associated companies' (ssap 1) was issued in january 1971. Any of a series of accounting standards prepared by the *accounting standards board and issued by the six members.

The object of these ssaps is first and foremost to ensure a degree of standardisation and uniformity in the preparation of accounts. Statements of standard accounting practice. What does statements of standard accounting practice (ssap) mean?

Statements of standard accounting practice (ssap) uk accounting standards developed by the predecessors to the financial reporting council (frc). Statements of standard accounting practice p. Statements of standard accounting practice are not intended to apply to immaterial items (see paragraph 8 of the foreword).

Accounting Standards Youtube

The Cover Letter For An Account Is Shown In This File, And It Appears

Chart Of Accounts Accounts, Accounting, Learn Accounting

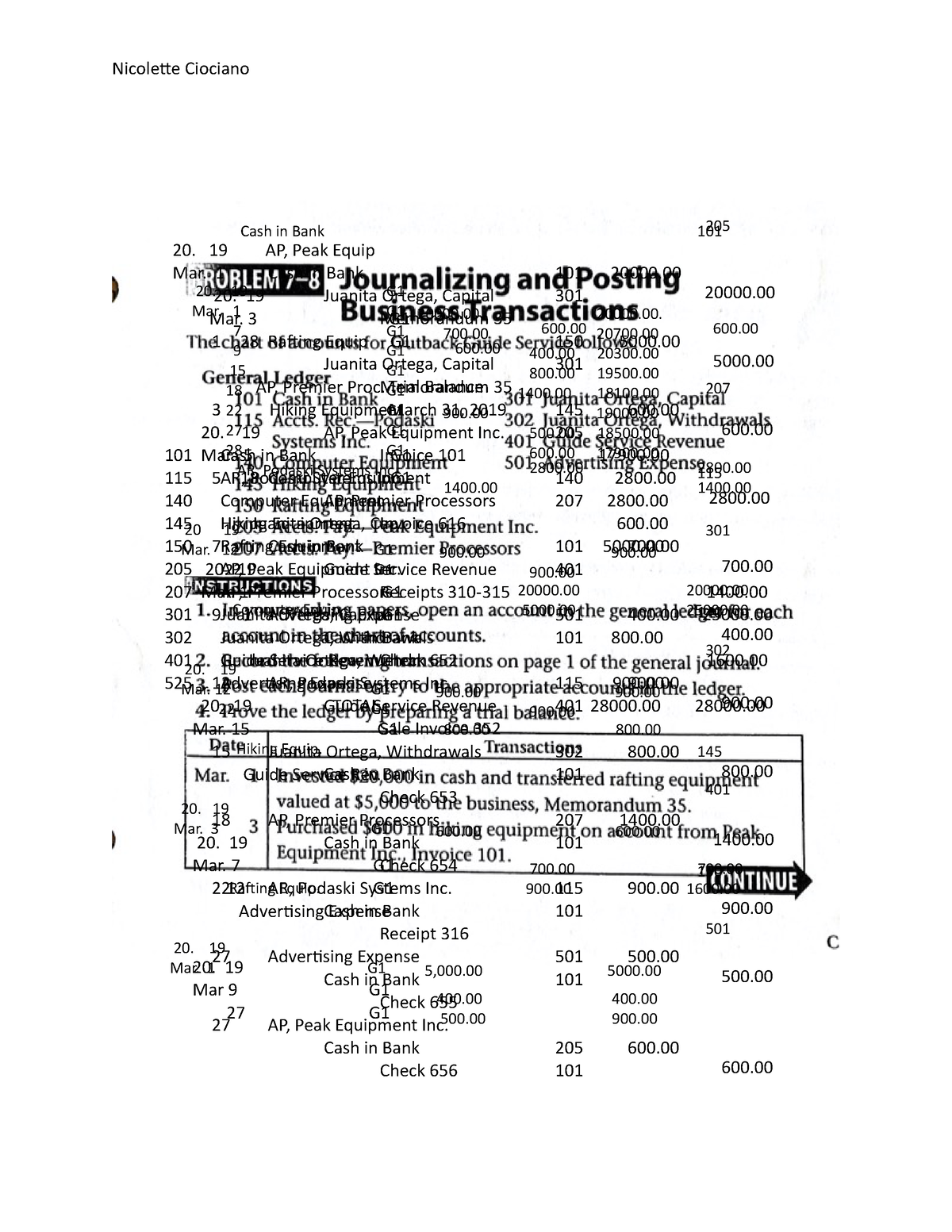

78 Accounting Practice 20000 20000. 700 20700. 400

Advanced Accounting Practice Notes Bbfa3034

Accounting Practice Assessment Youtube

Accounting Statement Of Purpose (500 Words)

Excel Retaining Original Table Formatting After A 'pagebreak' Stack

Advance In Financial Accounting Practice Quiz Accountancy Studocu

An Statement Is A Financial That Reports Company's

Revision Management Accounting Questions 1 Mang 6341

Accounting Concepts Typewriter Image