Glory Info About Steps For Preparing A Trial Balance

Preparing Trial Balance Youtube

Ppt List The Steps In Accounting Cycle Powerpoint Presentation

Understanding Trial Balance Uses, Types, And How To Prepare It.

What Is Trial Balance, Format, How To Prepare Balance

What Is A Trial Balance?

How To Make Trial Balance In Excel (with Easy Steps) Exceldemy

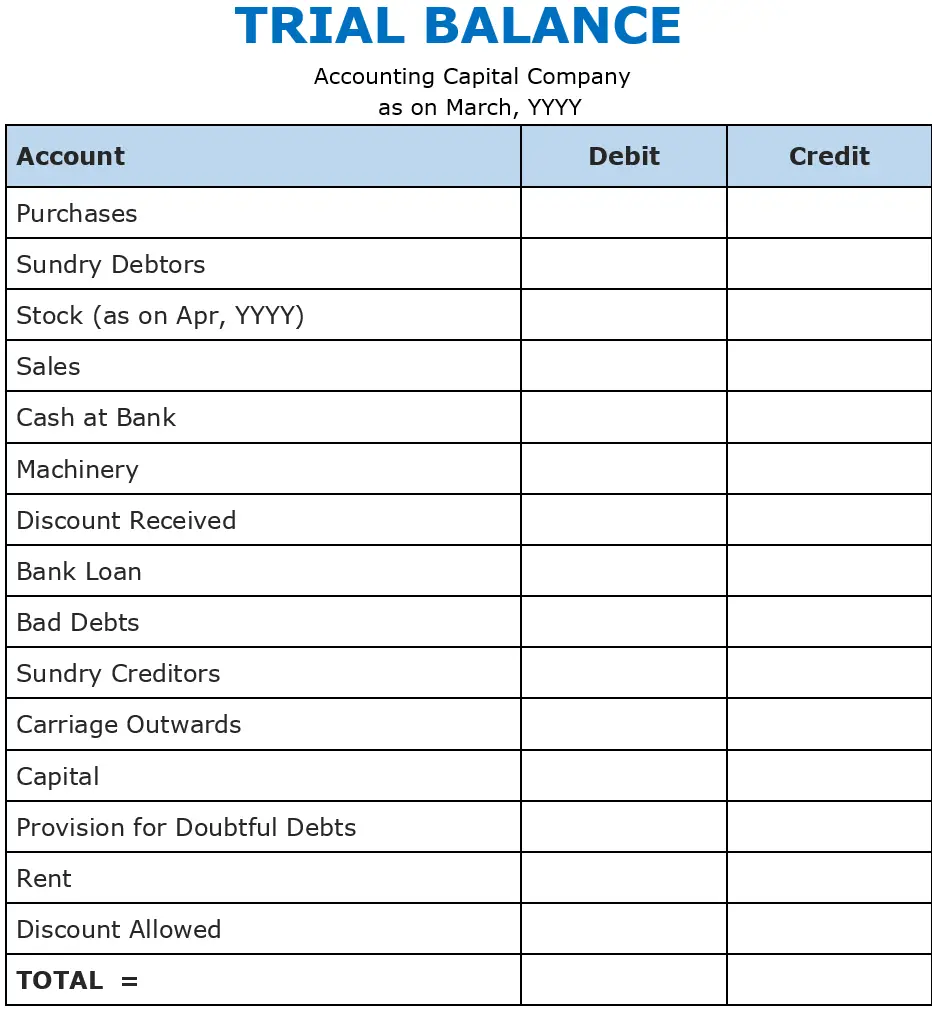

On the trial balance the accounts.

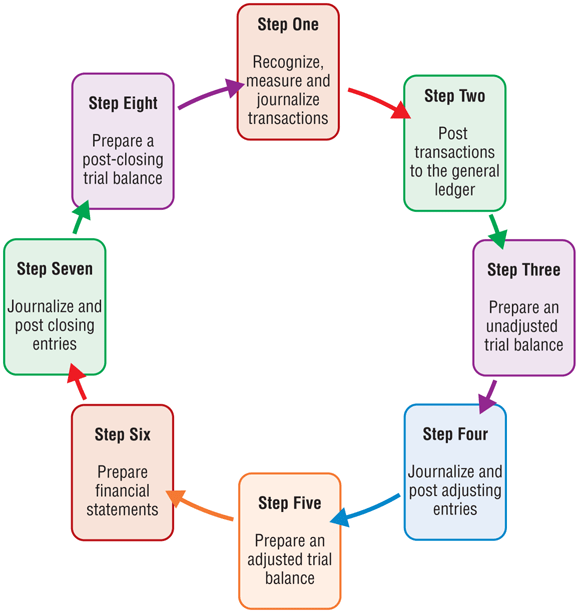

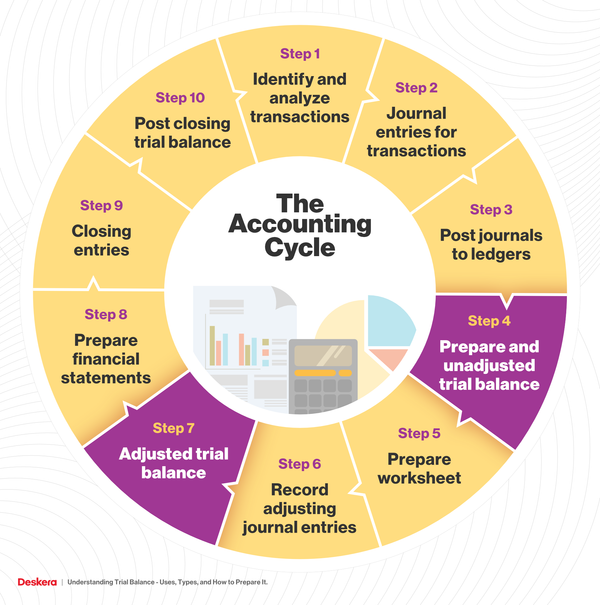

Steps for preparing a trial balance. Here are the steps involved in preparing the trial balance. The title of each general ledger account. Steps in preparing a trial balance step one;

The first step in the preparation of final accounts is the preparation of trial balance. All ledger accounts are closed at the end of an accounting period. The difference between debit and credit sums gives you the.

Steps for preparing the trial balance are: The trial balance is prepared after posting all financial transactions to the journals and summarizing them on the ledger statements. These balances can be prepared either manually or by using an accounting system on a computer.

Following steps are involved in the preparation of a trial balance: The basic purpose of preparing a trial balance is to test the arithmetical accuracy of the ledger. On the trial balance the accounts.

Although you can prepare a trial balance at any time, you would typically prepare a trial balance before preparing the financial statements. If all debit balances listed in the trial balance equal the total of. However, a business may choose to prepare the trial balance at the end of any specific.

Definition of a trial balance. The trial balance is made to ensure that the debits equal the credits in the chart of accounts. Preparing an unadjusted trial balance is the fourth step in the accounting cycle.

The following are the steps to take when preparing a trial. This report plays a vital role in consolidating,. Preparing a trial balance involves listing the ending balances of each account in the chart of accounts in balance sheet order.

Although you can prepare a trial balance at any time, you would typically prepare a trial balance before preparing the financial statements. So it is absolutely essential that we prepare the trial balance perfectly, so our final accounts do. For preparing a trial balance, it is required to close all the ledger accounts, cash book and bank book first.

Typically, trial balance is prepared at the end of an accounting year. Ledger balances are posted into the trial. To prepare a trial balance, you will need the closing balances of the general ledger accounts.

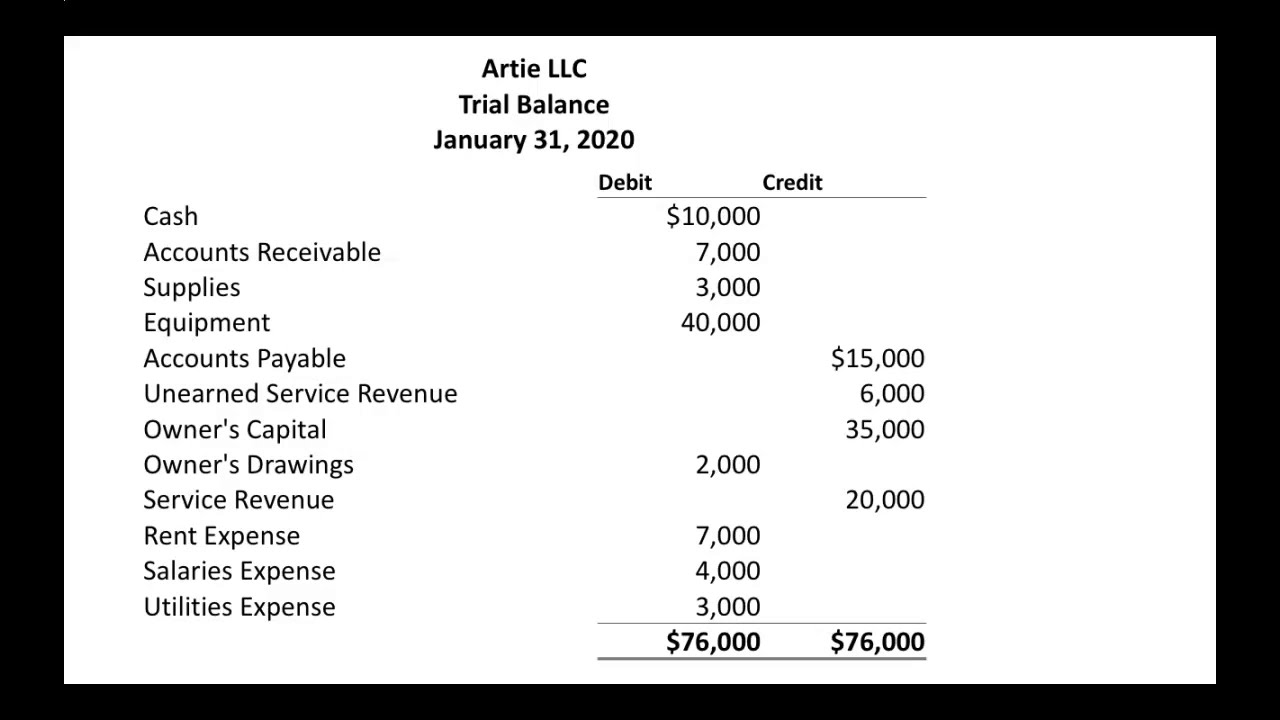

A trial balance consists of the following information: A trial balance is a list of all accounts in the general ledger that have nonzero balances. The first step is to make sure that all the ledger accounts are balanced.

Trial Balance Preparation Example Definition

How To Prepare A Trial Balance Accounting Cycle, Errors Reflected In

Procedure For Preparing A Trial Balance Everything About Accounting

Preparing Trial Balance, Statement, And Balance Sheet Youtube

What Is Trial Balance (with Format And Pdf) Accounting Capital

How To Prepare A Trial Balance Youtube

How To Prepare A Trial Balance In 5 Steps

Ppt Section 3 Preparing A Trial Balance Powerpoint Presentation

Fine Beautiful The Accounting Cycle Requires Three Trial Balances Small

![Procedure for Preparing a Trial Balance [Notes with PDF] Trial Balance](https://everythingaboutaccounting.info/wp-content/uploads/2020/01/Procedure-for-Preparing-a-Trial-Balance-1.png)

Procedure For Preparing A Trial Balance [notes With Pdf]

Trial Balance And Financial Statements Exercise Online Degrees

Trial Balance Meaning, Purpose, Sides, Sheet, Undetectable Errors, Etc

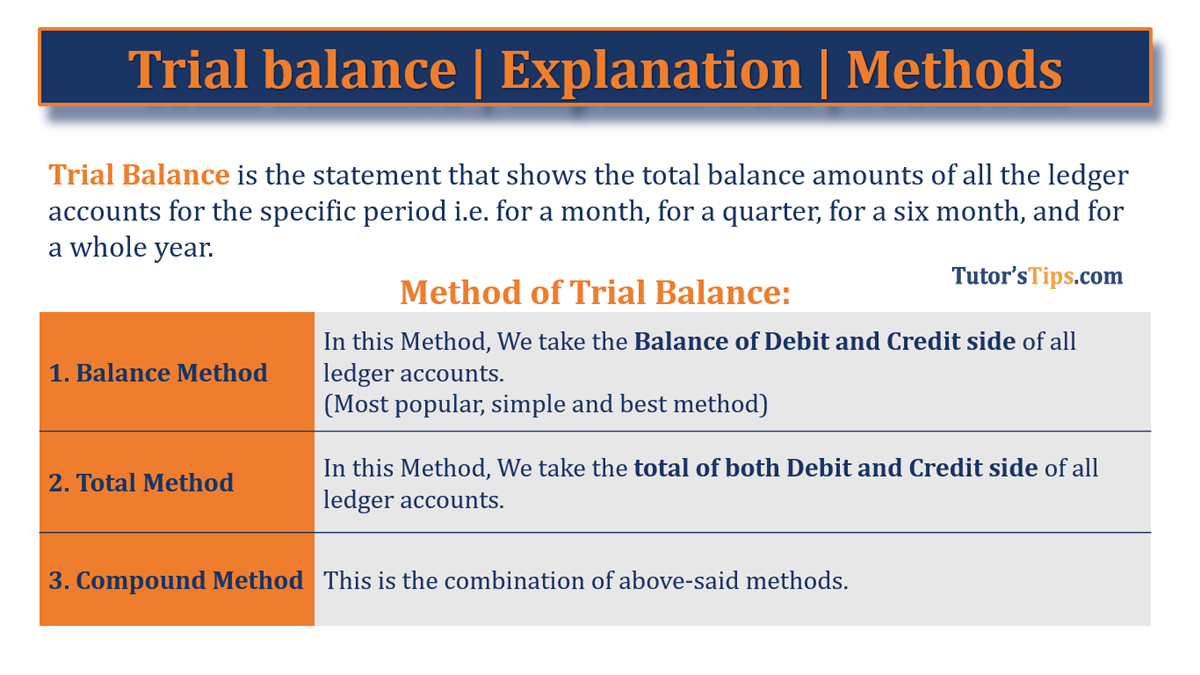

Trial Balance Explanation Methods Examples Tutor's Tips